[ad_1]

Key Findings

- One yr after the enactment of the Inflation Discount Act (IRA), the regulation’s difficult tax will increase on massive companies, notably the minimal tax on ebook revenue, have resulted in extraordinary implementation challenges and taxpayer confusion, with many questions left unresolved. Funds for each the minimal tax and the inventory buyback tax are at present on maintain till the IRS points additional steerage.

- The regulation’s subsidies for inexperienced vitality, within the type of a number of tax credit with novel options together with transferability and monetization, have confirmed enticing to taxpayers, resulting in escalating budgetary prices approaching $1 trillion over the subsequent decade. Amongst different issues, this implies the IRA as a complete possible worsens deficits.

- Congress ought to rethink key parts of the IRA, together with the ebook minimal tax and the inexperienced vitality credit, with an eye fixed in direction of simplification and financial accountability.

Introduction

On August 16th final yr, President Biden signed into regulation the Inflation Discount Act (IRA), probably the most substantial federal tax laws for the reason that Tax Cuts and Jobs Act (TCJA) of 2017.[1] The IRA is an formidable effort to attain a number of, competing objectives. Because the title implies, the regulation was meant to cut back inflation by decreasing deficits, primarily through new taxes on massive companies within the type of a minimal tax on monetary (or ebook) revenue, a inventory buyback tax, and an excise tax on drug corporations that allows the federal government to regulate drug costs. As nicely, the regulation gives a considerable enhance for the IRS funds, primarily to extend enforcement and tax collections.

The IRA was additionally meant to handle local weather change by way of large subsidies for inexperienced vitality on an unprecedented scale, primarily within the type of beneficiant and largely uncapped tax credit. As well as, most of the credit are designed to shift manufacturing to home sources, enhance unionized labor, and favor communities historically depending on fossil gasoline manufacturing.

As a byproduct, the IRA introduces a brand new set of complexities within the tax code, resulting in implementation challenges, reams of regulatory steerage and taxpayer feedback, and unresolved questions remaining greater than seven months after the regulation went into pressure.[2] The next evaluation gives a snapshot of what we all know concerning the IRA one yr after enactment when it comes to implementation of the main provisions, excellent taxpayer considerations, and financial and financial impacts.[3]

E book Minimal Tax

The brand new 15 % minimal tax on ebook revenue (also referred to as the company various minimal tax, or CAMT) isn’t so simple as it might sound. The 15 % minimal tax applies to company ebook revenue, with sure changes, for companies with income over $1 billion, efficient for tax years starting after December 31, 2022. As a brand new tax on a brand new tax base (adjusted monetary assertion revenue), it introduces a wide range of issues and unintended penalties, embroiling taxpayers and directors in a number of knotty points that stay unresolved. Implementation has been difficult and preliminary regulatory steerage launched by the Treasury Division and IRS addressed solely a restricted set of points, leaving extra questions than solutions for taxpayers and practitioners as detailed in a whole lot of pages of remark letters, a few of that are summarized beneath.[4]

Educational accounting and coverage consultants have been clear in warning concerning the risks of utilizing ebook revenue for tax functions.[5] Most of the challenges stem from the truth that monetary accounting and tax accounting serve completely different functions, the previous to supply info to shareholders and different traders on the monetary well being of corporations primarily based on requirements of monetary accounting and the latter to find out tax legal responsibility below the principles established by Congress. Squaring this circle is proving to be an awesome conundrum for the attorneys and economists on the Treasury Division and IRS tasked with drafting steerage for the ebook minimal tax (BMT), who’re extra acquainted with tax accounting than monetary accounting.[6]

One key distinction between tax and ebook accounting is the therapy of capital funding, reminiscent of tools purchases. For ebook functions, capital funding bills are depreciated and recorded over the lifetime of the asset, following the matching precept in accounting of matching bills with related revenue. For tax functions, Congress has lengthy acknowledged utilizing schedules that expedite depreciation deductions will improve incentives to take a position, resulting in many tax provisions for accelerated depreciation, reminiscent of Part 168(okay) bonus depreciation for short-lived property reminiscent of tools. Reflecting ongoing considerations about funding impacts, simply days earlier than the passage of the IRA, Congress amended the BMT to permit taxpayers to make use of tax depreciation slightly than ebook depreciation in willpower of adjusted monetary assertion revenue (AFSI) topic to the tax, however just for Part 168(okay) property.

Whereas the change decreased the financial hurt of the tax, it additionally added a considerable quantity of complexity and compliance price for taxpayers. E book accounting doesn’t monitor Part 168(okay) property, so taxpayers will probably be required to assemble and monitor the property individually, together with its tax foundation, utilizing ebook accounting asset classes. The method is additional difficult by the beginning date of the BMT (with the preliminary AFSI willpower interval starting in 2020), which penalizes taxpayers who utilized bonus depreciation previous to 2020.[7] Due to depreciation and different changes to monetary assertion revenue, taxpayers now need to maintain three units of books with the intention to adjust to the BMT: one for monetary functions, one for normal company tax functions, and one for the BMT.

One other main distinction between tax and ebook accounting is the therapy of features and losses on property. For tax functions, features and losses on property are usually decided primarily based on the conclusion precept, that’s, primarily based on a market transaction reminiscent of a sale. In distinction, monetary books typically monitor the unrealized features and losses of property on a mark-to-market foundation, which can lead to massive variations within the timing of revenue recognition. The statute and subsequent steerage acknowledged this mismatch in some however not all instances, permitting taxpayers to exclude from AFSI unrealized features and losses for sure property, reminiscent of these held in outlined profit pension plans. Taxpayers have famous this distorts funding selections by making a tax incentive to spend money on excluded property and have requested a complete exclusion from AFSI for all unrealized features and losses for ebook functions and different gadgets of revenue that aren’t included in common taxable revenue.[8]

A 3rd main distinction is that tax accounting is outlined by particular guidelines and restrictions whereas ebook accounting permits extra room for discretion and judgment calls on the a part of the corporate. One sensible implication in regard to the BMT is that the place there are ambiguities (and there are numerous), taxpayers will be capable of make ebook accounting selections that decrease tax legal responsibility. When the same tax was launched for 2 years within the Eighties, proof signifies corporations did in truth decrease ebook revenue in response to the tax.[9] As accounting and coverage consultants have famous, this results in basic questions concerning the soundness of the BMT as a income raiser or as a tax that ensures in any actual sense a sure stage of minimal tax. The identical consultants have additionally warned that by creating an incentive for taxpayers to govern monetary revenue to cut back tax legal responsibility, the BMT may undermine the credibility and usefulness of firm monetary info on which our capital markets rely.[10]

Taxing ebook revenue is resulting in a wide range of implementation challenges and taxpayer confusion past the areas of concern highlighted above. As with the problem of unrealized features and losses, regulatory steerage and taxpayer feedback thus far level to a number of points that could be unresolvable with out producing large compliance prices for taxpayers or limiting the tax in such a means that it fails to generate any substantial quantity of income for the federal authorities.[11]

As an example, one set of excellent points revolves round which monetary statements and requirements apply for reporting AFSI. For multinational enterprises and particularly inbound corporations (that’s, foreign-headquartered corporations with U.S. associates), a few of their operations might report monetary revenue below the U.S. accounting customary (Usually Accepted Accounting Ideas, or GAAP) whereas others might report revenue below the worldwide customary (the Worldwide Monetary Reporting Requirements, or IFRS). The statute signifies taxpayers ought to prioritize GAAP accounting over IFRS and different requirements, however that also leaves questions on find out how to match and mix the requirements for various operations on a consolidated foundation.[12]

A associated drawback is the mismatch between consolidation guidelines for ebook and tax revenue.[13] U.S. GAAP requirements consolidate entities in sure truth patterns the place tax doesn’t (e.g., partnerships could be consolidated below U.S. GAAP however not tax guidelines).[14] A selected problem with the BMT is that the present statute and steerage may end result within the double counting of revenue from majority-owned international companies (managed international companies, or CFCs); taxpayers have subsequently requested a broad exclusion of CFC dividends from AFSI.[15]

Insurance coverage corporations face a novel set of points and use a particular set of accounting guidelines, main the Treasury Division to launch 21 pages of particular steerage for the insurance coverage business that addresses a number of points and permits taxpayers to exclude many gadgets of revenue for BMT functions.[16] These questions will not be distinctive to the insurance coverage sector.

One other excellent set of points pertains to partnerships that move as much as companies topic to the tax.[17] The largest open query is when—and the way a lot—partnership revenue is required to be included by associated companies (direct company companions, oblique company companions, and companies which are a part of the identical managed group). Whereas the BMT is geared toward massive companies, because it stands, the regulation could be interpreted to require any partnership of any dimension to report if the partnership has any company companions. The duty is made tougher by the truth that many partnerships do not need audited monetary statements.

Then there’s the query of “distributive share.” The statute stipulates that “if the taxpayer is a companion in a partnership, adjusted monetary assertion revenue of the taxpayer with respect to such partnership shall be adjusted to solely consider the taxpayer’s distributive share of adjusted monetary assertion revenue of such partnership.” Nonetheless, “distributive share” is a tax idea that doesn’t neatly apply to ebook revenue, elevating many unanswered questions. Preliminary regulatory steerage (which offered 50 pages of steerage on many points) didn’t resolve these and different challenges with partnerships, reminiscent of find out how to take care of tiered partnerships.[18] Because it stands, company companions might must request from the partnership info on AFSI or the IRS may rule that partnerships are required to supply that info, doubtlessly ensnaring 1000’s of partnerships in a brand new reporting requirement and compliance burden of unknown scale.[19]

Taxpayers are additionally involved about one-time actions pushing them over the $1 billion revenue threshold that determines if they’re topic to the ebook minimal tax. Such actions may embody a sale of a enterprise unit or different merger and acquisition actions. Steering up to now has addressed find out how to deal with sure transactions, reminiscent of spin-offs, however questions stay concerning the therapy of different extraordinary transactions. Whereas the brink is set primarily based on a three-year common of revenue, taxpayers have complained that that is “not an efficient nor honest measure” because of the volatility of their revenue.[20] Some taxpayers have requested the choice to drop one yr from the three-year common or in any other case disregard extraordinary transactions.[21] These issues are particularly necessary as a result of as soon as a taxpayer is topic to the ebook minimal tax, the taxpayer stays topic to it eternally no matter revenue (however the Treasury Secretary can grant exceptions). A further drawback with the $1 billion threshold is the shortage of inflation indexing, so over time extra corporations will probably be swept in (the value stage has already elevated about 3 % for the reason that passage of the tax, as measured by the Client Value Index).

Remark letters from taxpayers and practitioners determine quite a few different particular points with the BMT, typically disagreeing on how greatest to resolve them.[22] As an example, the American Bar Affiliation and New York State Bar Affiliation agree the preliminary steerage ought to change concerning foundation adjustment guidelines to find out whether or not monetary accounting or tax guidelines apply for recognition of acquire or loss in some reorganization transactions, however varied factions come to completely different conclusions on find out how to deal with it. Associated to that’s the problem of how far again to look to make changes for revenue and asset foundation. Tax attorneys usually agree there ought to be a restricted look-back interval however don’t agree on a time-specific restrict. Concerning the secure harbor rule specified within the preliminary steerage, which permits sure corporations to keep away from the tax in 2023 utilizing a simplified willpower, tax attorneys usually agree with the rule however request that it’s made extra broadly relevant and prolonged completely.

Lastly, within the newest announcement on June 7, the IRS granted penalty aid for companies that don’t pay estimated tax for 2023 associated to the ebook minimal tax, as a consequence of “challenges related to figuring out whether or not a company is an Relevant Company and the quantity of a company’s CAMT legal responsibility.”[23]

It’s not clear when the IRS will present extra steerage or to what diploma it’d deal with the problems raised in remark letters. In March of this yr, an IRS official described the regulatory course of for the BMT as “an extended slog” whereas a Treasury official indicated plans to launch “extra detailed and refined proposed laws later this yr.”[24]

Buyback Tax

In comparison with the ebook minimal tax, the tax on internet share repurchases (or buybacks) is comparatively easy. The statute requires a 1 % excise tax relevant to publicly traded corporations on the worth of their inventory repurchases through the taxable yr, internet of recent issuances of inventory, for repurchases after December 31, 2022. The tax excludes inventory contributed to retirement accounts, pensions, and worker inventory possession plans (ESOPs). Subsequent steerage launched a controversial rule that significantly expands the scope of the tax to use to share repurchases by foreign-headquartered corporations with U.S. associates.

The statute signifies that if a U.S. firm buys the inventory of its public international affiliate, then the excise tax may apply. Whereas such a state of affairs is uncommon, steerage issued in December expanded the scope of the tax to incorporate, in lots of instances, share repurchases made by international corporations with U.S. associates (inbound corporations).[25] The steerage achieved the enlargement by creating a very broad funding rule. The rule gives that if the U.S. firm “funds” its international affiliate by sending funds for practically any purpose inside two years of a inventory repurchase by the international affiliate, the tax applies to that inventory repurchase. Cross-border funds that might set off the tax embody funds for widespread enterprise providers, reminiscent of curiosity funds, royalties, stock purchases, and funding for an in-house financial institution.

Remark letters from foreign-headquartered corporations level to the risks of the ruling, together with reciprocal actions from international governments that might flip round and tax U.S.-based multinational enterprises (MNEs) in the identical means.[26]

Maybe acknowledging these considerations, on June 29, the IRS issued steerage indicating taxpayers will not be required to report the buyback tax on their tax return or make any funds of the tax till additional steerage is issued, recommending within the meantime that taxpayers maintain data for share repurchases made after December 31, 2022.[27] It’s not clear when additional steerage could also be issued, however the normal expectation is that it’ll possible arrive earlier than the top of this yr and can make clear the funding rule to be extra in keeping with the statute.

Clarifying the funding rule will get rid of a lot of the remaining uncertainties concerning the tax, however it is not going to get rid of the tax’s distortionary results. As many coverage consultants have famous, the tax is geared toward discouraging corporations from distributing extra money to shareholders within the type of buybacks, however it’s not in any respect clear why this habits ought to be punished. Corporations can distribute money to house owners by way of dividends or buybacks, and firms have authentic causes for selecting one or the opposite.

For instance, whereas dividends are usually used for normal distributions, buybacks present a level of flexibility for the corporate and a method to problem one-time distributions with out creating shareholder expectations that they’ll proceed.[28] No proof exists to point buybacks come on the expense of funding; as a substitute buybacks enable corporations to launch extra money in an environment friendly method, permitting shareholders to recycle funds into different investments.[29] The brand new buyback tax, as soon as totally applied and enforced, will interrupt and warp the environment friendly and useful means of recycling investable funds, resulting in fewer buybacks together with some mixture of elevated dividend payouts and inefficient use of funds by corporations.[30]

Inexperienced Power Tax Credit

One of the crucial formidable elements of the IRA is the enlargement or creation of twenty-two tax credit for inexperienced vitality improvement and use, subsidizing varied applied sciences associated to zero-carbon vitality era, electrical automobiles, residential clear vitality, various fuels, and superior manufacturing.[31] The credit have two main objectives: growing the event and deployment of low- or zero-emission applied sciences and growing funding and development within the U.S. financial system broadly.[32]

The IRA credit could be sorted in line with typical emissions sectors: utility-level electrical energy and energy era, transportation, industrial and residential buildings, and industrial actions.[33]

Energy Sector Credit

The 5 tax credit geared toward decreasing emissions within the energy sector scale back uncertainty in tax breaks for inexperienced vitality in some methods. Provisions such because the vitality manufacturing credit score and vitality funding credit score was once extenders requiring renewal nearly yearly. Now, many of the new inexperienced insurance policies will probably be in place for 10 years. The longer availability stabilizes incentives for corporations to make funding selections, avoiding the uncertainty related to the year-end push to increase expiring provisions.[34]

It is usually value clarifying that the IRA prolonged and expanded current credit for clear vitality funding (Part 48) and manufacturing (Part 45) till the start of 2025. Beginning in 2025, the IRA’s new manufacturing and funding credit (Part 45Y and Part 48E, respectively) will successfully exchange the pre-existing credit with an improved technology-neutral coverage. The IRA additionally launched a tax credit score (Part 45U) for current nuclear energy manufacturing.

However the IRA’s new credit have include new complexities. Many pair stability concerning incentives with complexity inside the incentives themselves. As an example, the brand new energy credit embody bonus credit for paying prevailing wages (geared toward boosting unionized labor), establishing apprenticeships, assembly home content material necessities, and finding actions in communities traditionally house to substantial fossil gasoline business.

The contingencies have necessitated extra steerage from the IRS. In November 2022, the IRS printed steerage on the wage and apprenticeship necessities, primarily affecting the ability era sector.[35] In February 2023, the IRS printed preliminary steerage on the vitality neighborhood and low-income neighborhood bonus credit and issued new or up to date steerage in April and June as nicely.[36] The company printed preliminary steerage for the home content material bonus credit in Could 2023, with explicit consideration for what qualifies as domestically produced.[37]

One other problem related for the ability sector credit (in addition to for a number of different insurance policies) is direct pay and transferability. Tax credit are used to offset tax legal responsibility, however some entities haven’t any current tax legal responsibility to offset, reminiscent of startup corporations not but worthwhile or nonprofit and governmental entities. To make the IRA incentives out there to such entities, the IRA permits credit to be bought to different taxpayers with tax legal responsibility (transferability) or for direct funds to be made when it comes to the worth of the credit score. This coverage alternative has necessitated extra steerage.[38] Transferability additional blurs the road between tax credit and authorities spending. Whereas it is going to create extra incentives for untaxed entities to spend money on inexperienced vitality, it may additionally result in vital compliance and administrative challenges for each taxpayers and the IRS.[39]

Transportation Sector Credit

9 credit are geared toward decreasing emissions from the transportation sector. Many of the subsidies for transportation give attention to decreasing emissions from highway journey, predominantly by subsidizing electrical automobiles (EVs) (Part 30D, Part 25D, and Part 45W) and EV infrastructure (Part 30C). Nonetheless, others give attention to various fuels like biodiesel (Part 40, Part 40A, Part 40B, Part 45Z).[40] Lastly, Part 45V gives a tax credit score for clear hydrogen know-how, which has the potential for quite a few purposes throughout sectors, however most prominently transportation.[41]

The a number of tax credit associated to EVs have been on the middle of compliance challenges and controversies. For one, the eligibility for EV credit is partly contingent on the manufacturing location of important minerals and battery elements, to not point out manufacturing of the automobiles themselves.[42] The home content material necessities led to vital tumult internationally, notably from the European Union, South Korea, and Japan.[43]

Over the previous yr, the administration has slowly tweaked the credit to make them extra out there for foreign-produced vehicles. In December 2022, steerage made foreign-made automobiles eligible for the industrial car credit score, so long as the automobiles had been leased. In late March and early April of 2023, offers with South Korea and Japan primarily happy the home content material requirement for vehicles they produced.[44] The U.S. and EU might but attain an settlement concerning eligibility of EU-produced vehicles, however negotiations are at an deadlock.[45]

The lengthy sequence of IRS steerage illustrates the complexities of the EV credit. In December 2022, the IRS issued the primary set of notices and an FAQ web page, adopted by one other replace in February.[46] The IRS additionally launched steerage for industrial clear vitality automobiles on the finish of December 2022, later updating the rules in February 2023.[47] Whereas these publications have helped taxpayers navigate these complicated credit, future coverage modifications due to negotiation with European nations might necessitate one other spherical of steerage.

Business and Residential Buildings Credit

4 provisions are focused at emissions produced inside houses and companies.

Two credit are centered on households. The nonbusiness vitality property credit score (Part 25D) covers 30 % of the set up of residential-level vitality property, reminiscent of photo voltaic panels, geothermal warmth pumps, and small wind generators.[48] The vitality effectivity enhancements credit score (Part 25C) covers 30 % of prices for varied house building parts and home equipment. Beforehand, taxpayers confronted a $500 lifetime restrict, however the IRA raised the utmost worth to $1,200 per yr and eliminated lifetime limits.[49] The IRA additionally tweaked qualifying expenditures for every credit score.[50]

In the meantime, the opposite tax provisions associated to constructing sector emissions are extra centered on companies. The credit score for the development of recent housing items that meet sure vitality effectivity necessities (Part 45L) is allotted to building contractors.[51] The Power Environment friendly Business Buildings Deduction (Part 179D) gives an additional tax deduction for vitality effectivity enhancements in industrial buildings, which helps compensate for general poor tax therapy of vitality effectivity enhancements and buildings funding in some methods.[52] However like many different insurance policies within the IRA, the motivation options substantial bonuses for prevailing wages.[53]

Industrial and Miscellaneous Credit

The opposite main class of CO2 emissions is industrial emissions, the place varied industrial processes, reminiscent of cement manufacturing, launch CO2 and different greenhouse gases as a byproduct. Relatively than give attention to emissions, the tax credit immediately utilized to industrial manufacturing are extra involved with onshoring industrial manufacturing of varied inexperienced vitality elements.

The IRA additionally expanded the present tax credit score for carbon sequestration, each the values offered per ton of CO2 captured for various actions and the eligible amenities.[54] Like many different credit, the extra worth of the credit score is contingent on prevailing wage necessities. This element has led to some uncertainty, as carbon sequestration know-how is commonly connected to an current facility that will not have been constructed with the prevailing wage necessities of the credit score.[55]

The IRA’s credit score for certified superior vitality tasks (Part 48C) has a number of notable options. It gives a base credit score of 6 % of prices for clear vitality challenge manufacturing and recycling, emissions discount tasks within the industrial manufacturing sector, and the manufacturing of specified important minerals. The credit score can then be boosted to 30 % by assembly a number of circumstances reminiscent of prevailing wage and home content material necessities.[56]

Part 48C can also be notable for the way it blurs the road between tax credit score and grant program, because it requires tasks to undergo an software course of.[57] Not like different credit, that are largely uncapped, the superior vitality property credit score is proscribed to $10 billion, to be allotted by the IRS. Moreover, the credit score can solely be claimed as soon as, and a minimum of $4 billion of the credit score have to be allotted to current vitality communities, per preliminary and subsequent steerage issued in February and Could.[58]

The superior manufacturing manufacturing credit score (Part 45X) is focused at important mineral manufacturing, in addition to the manufacturing of different inexperienced vitality merchandise and elements. The credit score is value 10 % of the price of manufacturing of an extended sequence of minerals.[59] Notably, it’s not to be confused with the Superior Manufacturing Funding Credit score launched within the CHIPS Act of 2022.[60] Relative to Part 48C, Part 45X is a extra standard tax credit score.

Fiscal Influence

The fiscal influence of the IRA inexperienced vitality credit appears like it will likely be a lot bigger than initially anticipated. When the Joint Committee on Taxation (JCT) reassessed the income price in Could 2023, they discovered a tough doubling for the reason that regulation’s enactment: from 2023 to 2031, they discovered a $536 billion price in comparison with the unique $271 billion price.[61] Specifically, the Superior Manufacturing Manufacturing Credit score, the modified vitality credit score, and the EV credit noticed massive will increase in estimated prices, with all of them greater than quadrupling. JCT attributes the expansion to a number of elements together with Treasury’s expansive steerage in addition to will increase in anticipated manufacturing capability for batteries and renewable vitality. JCT additionally offered estimates over an extended funds window, discovering the credit price $663 billion over the interval 2023 to 2033.

JCT’s evaluation has not factored in current local weather efforts by authorities businesses that might push price estimates increased.[62] For instance, the Environmental Safety Company (EPA) has lately proposed guidelines that mandate stricter emissions requirements for brand new automobiles beginning in 2027, successfully requiring a serious shift to EVs.[63] The EPA estimates the brand new laws may add as a lot as $210 billion in tax income losses between 2027 and 2032: $136 billion from EV credit and $74 billion from the battery manufacturing credit score.[64]

Analyses by a number of different organizations additionally level to escalating fiscal prices. For instance, the Penn-Wharton Finances Mannequin estimates the mixed vitality and local weather provisions within the IRA will price about $1 trillion over the subsequent decade, whereas Goldman Sachs places the fee at about $1.2 trillion.[65] A research by students on the Brookings Establishment finds the fiscal price by way of 2031 may vary from $244 billion to $1.1 trillion relying on assumptions about eligibility and provide constraints.[66]

Financial Influence

The rising fiscal prices of the IRA credit mirror growing taxpayer curiosity, uptake, and doubtlessly bigger financial results than initially anticipated. Basically, tax credit for particular varieties of funding ought to have two results. First, the general common tax burden on funding ought to fall, incentivizing extra funding. Second, the relative worth of various investments ought to change, inflicting funding to shift from unsubsidized sectors to newly backed sectors.

Because the passage of the IRA, now we have seen substantial new investments in backed sectors and industries, however no clear signal of a broad improve in funding economy-wide.[67] Extra information will probably be required, however even with years of knowledge, it will likely be troublesome to isolate the influence of the IRA’s tax modifications, notably on general funding, as a consequence of confounding coverage developments and financial elements.

For instance, as talked about, stricter emissions requirements for brand new vehicles, which have been pursued by the Biden administration since early 2021, have additionally inspired funding in EVs. The CHIPS Act, enacted in 2022, gives vital funding subsidies for sure industries. Then again, the Federal Reserve has considerably hiked rates of interest over the past yr and a half whereas taxes on enterprise funding have elevated (e.g., because of the phaseout of bonus depreciation and the requirement to amortize analysis and improvement [R&D] bills as specified within the TCJA).

The development in direction of inexperienced vitality funding and adoption of cleaner applied sciences predates the IRA. A decades-long sequence of technological enhancements have steadily improved the standard and lowered costs of key applied sciences reminiscent of batteries and photo voltaic panels, making widescale adoption and deployment far more possible even with out extra subsidies. As such, it’s unclear to what diploma the IRA credit have added to the development by boosting marginal incentives or if they’ve merely backed applied sciences that may have been developed anyway.

Moreover, funding in itself isn’t a coverage success. The purpose of funding is to extend productiveness, which ought to then result in will increase in wages and residing requirements. Often, we could be assured that every a part of this chain will maintain up. Within the IRA’s case, although, now we have good causes to be involved. Concentrating on all the tax advantages to some industries may end in a glut of funding that in the end proves to be unproductive. Then again, the tax credit may speed up technological improvement due to “studying by doing”; whereas, initially, some funding will not be notably productive, elevated exercise within the sector may spur productiveness enhancements.[68]

Drug Pricing

The IRA imposed a brand new coverage, the “Drug Value Negotiation Program,” to enable the federal government to find out a “most honest worth” corporations can cost for sure pharmaceuticals inside Medicare. If pharmaceutical corporations don’t adjust to government-set costs, they’ll face steep excise taxes starting from 186 % to 300 %, 567 %, or 1,900 % on their drug gross sales, relying on the period of time out of compliance.

Official estimates of the brand new regulation point out an expectation that each one producers would adjust to the government-set costs slightly than pay the excise tax penalties, in order that the tax itself doesn’t increase any income. Producers can also reply in different, unintended methods, together with pulling a drug out of the U.S. market, refocusing improvement on medicine which are much less more likely to be a prime Medicare drug, or different operational changes to cut back or keep away from being caught up within the drug pricing program.[69]

Every year, the federal government will choose from a listing of fifty medicine with probably the most spending in Medicare Half B and 50 in Medicare Half D. Eligible medicine embody single-source small molecule medicine which were available on the market for seven years and biologics which were available on the market for 11 years.

In 2023, the federal government can choose from the checklist the primary 10 medicine to face worth restrictions, which can kick in beginning in 2026. In 2025 and 2026, the federal government can choose one other 15 medicine every year, after which it could choose 20 medicine per yr. Whereas worth controls solely apply to Medicare Half D in 2026 and 2027, afterward they’ll apply to Half B as nicely.

Forcibly decreasing costs will scale back prescription drug spending, saving the federal government cash by decreasing expenditures inside Medicare. However it is going to additionally scale back investments in biopharmaceutical R&D that produce new medicine and discover new purposes for current medicine. For instance, the Congressional Finances Workplace estimated that earlier variations of the drug pricing laws would trigger a 5 % discount in innovation, that means 8 to fifteen fewer medicine coming to market over the subsequent decade.[70] Outdoors estimates put the quantity a lot increased, suggesting CBO’s estimate is a decrease sure for potential innovation losses.[71]

Preliminary anecdotes point out the anticipated loss in innovation is already happening, as a number of drug corporations have introduced curtailment of varied drug improvement tasks, pointing to the brand new regulation.[72]

The Facilities for Medicare & Medicare Providers (CMS) issued its steerage on March 15, 2023, lower than six months earlier than the deadline for drug producers to signal agreements with CMS, with feedback due by June 20, 2023.[73]

In line with the remark solicitation letter, “So as to facilitate the well timed implementation of the Negotiation Program, CMS is issuing steerage on part 30 of this memorandum as last, with no remark solicitation,” save for a small exception inside that part. Part 30 is said to how CMS will determine, rank, and choose the negotiation-eligible medicine for 2026 worth restrictions, and never permitting public touch upon that basic part of this system is extremely questionable.

The tight timeline, issuing a serious part of steerage as last, and the consequences the drug pricing coverage will in the end have on innovation, drug improvement, and affected person entry, all illustrate the misguided method the IRA took to cut back Medicare spending. Whereas Medicare reform ought to be on the desk as lawmakers deal with debt, deficits, and inflation, lawmakers ought to discover different coverage choices.[74]

IRS Funding

The IRA included a considerable funding improve for the IRS to make use of from Fiscal Yr 2022 to Fiscal Yr 2031. The funding could be damaged into 4 classes: enforcement, operations help, enterprise system modernization, and taxpayer providers.

The spending will also be divided into completely different classes primarily based on coverage purpose. Within the IRS’s Strategic Working Plan, launched this April, the company introduced 5 goals for the funding package deal, in addition to a separate merchandise for implementing the IRA’s inexperienced vitality credit. Every goal entails funding from a number of spending classes. As an example, the purpose to “ship cutting-edge know-how, information, and analytics” contains funds from each the Enterprise System Modernization and Operations Assist account.[75]

In the end, the IRS funding package deal has two core objectives, with a number of the listed goals serving each.[76]

The primary purpose is bettering IRS customer support. IRS customer support was already poor earlier than the COVID-19 pandemic. It additional deteriorated as lawmakers saddled the company with administrating a number of large financial aid applications through the pandemic.

The second purpose is elevating income by bettering enforcement, thus decreasing tax noncompliance. Lowering noncompliance would chop the tax hole (the distinction between taxes legally owed and taxes collected) and assist fund the inexperienced vitality subsidies included within the IRA. Funding for workforce improvement and technological upgrades may assist serve each core objectives.[77]

Implementation so Far: Taxpayer Providers and Administrative Challenges

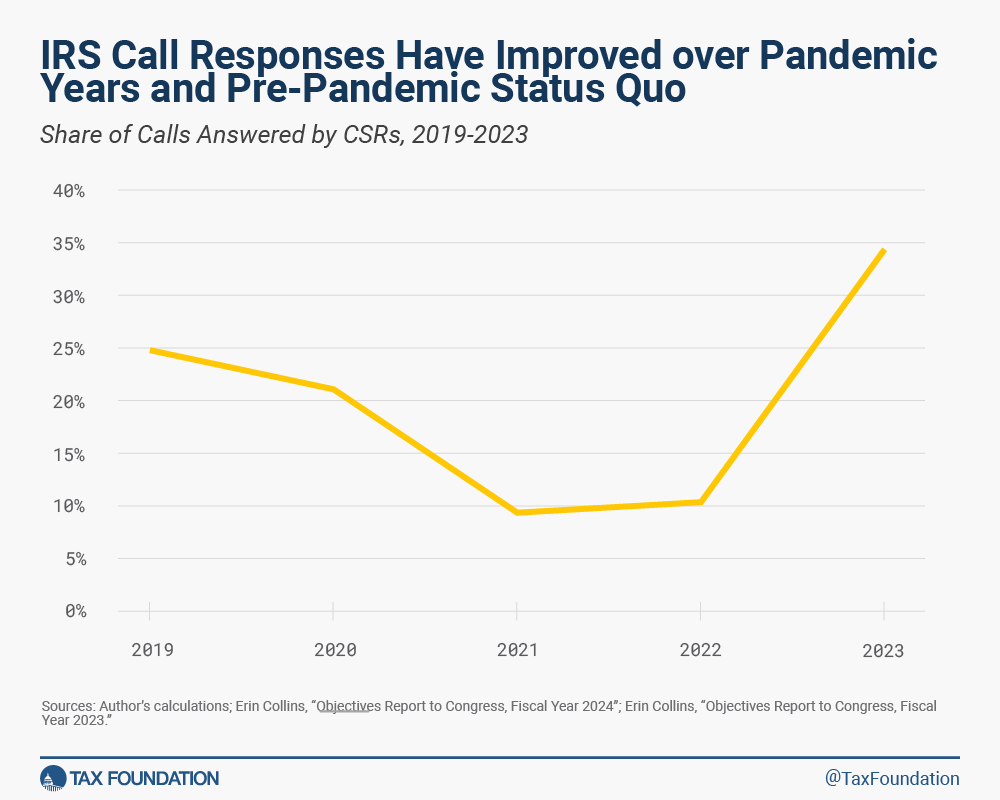

Taxpayer service has considerably improved within the 2023 submitting season. One of the crucial salient examples of service woes was unresponsive phone help. Customer support response charges sunk to roughly 10 % within the two tax seasons previous the IRA’s passage. Responsiveness improved through the 2023 tax season, after the company used new funds to rent 5,000 new customer support staff.

Throughout the 2023 tax season, IRS customer support brokers answered over 34 % of incoming calls in comparison with roughly 10 % of calls in 2021 and 2022 and 25 % of calls in 2019, the final pre-pandemic tax season.

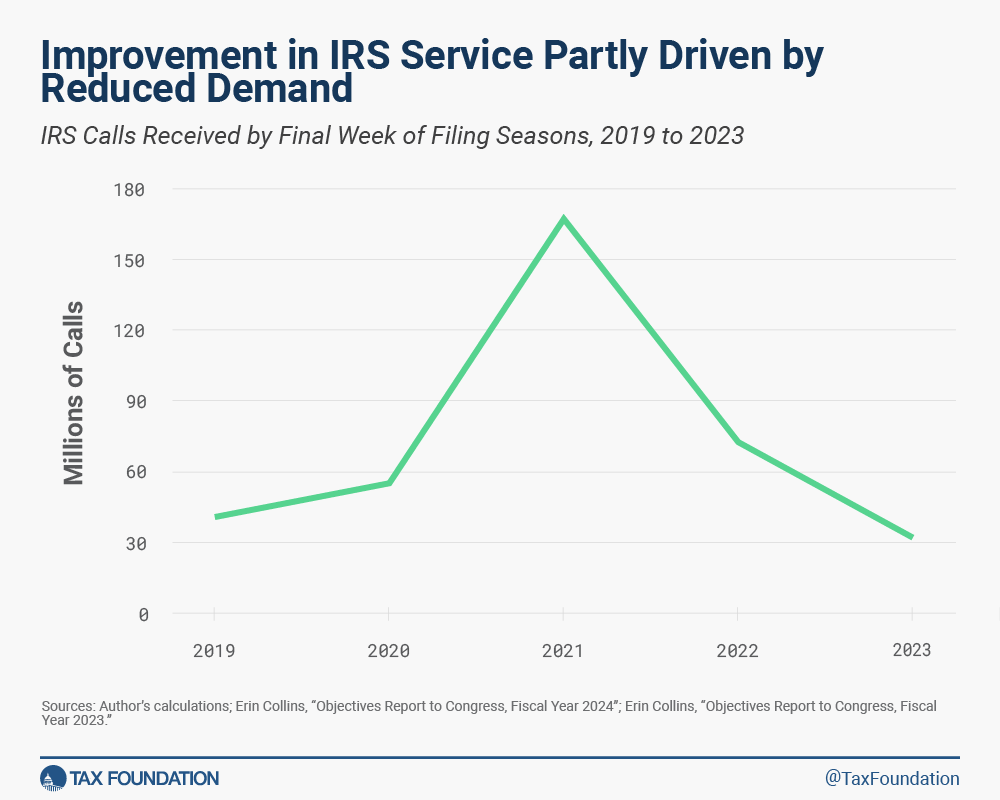

It’s value noting that some customer support enhancements have been as a consequence of decreased demand, not elevated capability. In 2022, pandemic-era aid applications, most notably the expanded Youngster Tax Credit score, expired, that means fewer questions and decreased demand for IRS service. Calls to the IRS fell by greater than 50 %, from nearly 73 million within the 2022 tax season to simply 32 million within the 2023 tax season.

One other indicator of the IRS’s service deficiencies is the backlog of paper returns. Nationwide Taxpayer Advocate Erin Collins has described paper tax returns, nonetheless submitted by thousands and thousands of taxpayers, because the IRS’s kryptonite.[78] A 2022 story from The Washington Publish vividly documented the laborious and comically outdated strategies the IRS makes use of to course of paper tax returns.[79] On the finish of the 2022 tax submitting season, the IRS was nonetheless processing some paper returns filed through the 2021 calendar yr and had a complete of 13.3 million paper returns and 29.1 million gadgets of correspondence awaiting guide processing.[80]

The IRS has considerably cleared up their backlog for the reason that IRA’s passage. By the top of the 2023 submitting season, the IRS had utterly cleared its 2022 backlog, and had simply 2.6 million remaining paper returns awaiting processing. Moreover, it had a complete stock of 16.9 million gadgets of correspondence awaiting guide processing, over a 40 % drop. This progress is principally because of the extra employees out there to course of returns, though some know-how enhancements have helped as nicely.[81]

Most metrics present that the IRS has delivered on improved service, even when helped by a post-pandemic decline in demand, however some regarding indicators stay.

The primary is a misallocation of assets geared toward juicing service particular metrics. As famous within the Nationwide Taxpayer Advocate’s midyear report, the elevated give attention to phone responsiveness has led to a buildup of amended returns awaiting processing.[82]

The second and extra regarding issue is the speed at which the IRS has burned by way of the brand new service funding. In line with the Strategic Working Plan, the company will exhaust its new service funding inside 4 years if it maintains present stage of service.[83]

The IRS’s Strategic Working Plan additionally gives a transparent illustration of the executive challenges the IRA credit have created. Within the April report, the IRS requested a further $3.9 billion in funding to additional implement the IRA’s inexperienced vitality credit, because the credit’ administrative price is consuming into the power to fund different goals, reminiscent of elevated enforcement and improved customer support.[84]

Relative to taxpayer service, enforcement effectiveness is tougher to measure. To begin, the Congressional Finances Workplace (CBO) didn’t predict that the extra enforcement funding would increase extra income within the subsequent couple of years because of the time required to recruit and practice new staff and to improve know-how.[85] The CBO estimated that the IRS enforcement provisions of the IRA would increase simply $2 billion in income in 2023 and $5.1 billion in 2024, that are marginal modifications within the context of a tax hole typically estimated to be close to or above $500 billion per yr.[86] Nonetheless, in later years, the figures are extra spectacular: CBO estimates that the improved IRS enforcement actions would increase a further $35 billion in income in 2030 alone.[87]

The IRS’s Strategic Working Plan highlights the event time wanted for its enforcement initiatives to take impact. For nearly each initiative below the target “Focus Enforcement on Taxpayers with Advanced Tax Filings and Excessive-Greenback Noncompliance to Deal with the Tax Hole,” the fiscal yr 2023 purpose is to rent and onboard new specialists and start the method of elevating audit charges, notably for big companies, partnerships, and high-wealth people, with refining of operational methods coming in future years.[88]

Subsequent yr, the IRS will launch information concerning audits in Fiscal Yr 2023, which can present some perception into how audit charges have elevated on the company and the extent to which “beneficial extra tax”, i.e., will increase in taxes owed ensuing from the audits, modified within the first tax season of expanded IRS funding.[89] Given the time it is going to take to ramp up enforcement efforts, we might nonetheless not anticipate a considerable bump in extra income till just a few years down the road.

The IRS publishes tax hole estimates with an extended lag. In 2022, it printed an evaluation of the tax hole for 2014 by way of 2016 with estimates for the hole in 2017 by way of 2019. Provided that we do not need estimates of the tax hole for present years, it might be a while earlier than we will consider the consequences of enforcement modifications on the tax hole with any diploma of certainty.[90]

Additional complicating the implementation of the IRS’s enforcement agenda, the current debt ceiling deal repurposed round $20 billion of the $80 billion funding improve the IRA granted the IRS, whereas outright reducing $1.4 billion.[91] It seems taxpayer service funding will probably be spared from the discount, that means that the deliberate enforcement expansions could also be curtailed. For now, the IRS has stated it is going to proceed with its funding plans, however until the funds are restored, the plans might have to be consolidated.[92] The IRS has not specified which goals or initiatives could also be in danger because of the approximate 25 % discount of its funding.

The jury continues to be out on the influence of the IRS funding improve in its totality. Essentially the most informative information out there thus far present that the IRS has made progress in bettering customer support, however that they could want extra funds to take care of the improved stage of service going ahead.

Conclusion

Enacted one yr in the past and now in varied phases of implementation, the IRA represents an formidable effort to attain a number of, competing objectives with various ranges of success. The purpose of deficit discount, and subsequently inflation discount, is most clearly off beam. The most effective proof signifies the regulation is growing deficits, doubtlessly by a whole lot of billions of {dollars}, as a consequence of explosive development in price estimates for the inexperienced vitality credit.[93] Moreover, two of the regulation’s main income raisers, the ebook minimal tax (BMT) and inventory buyback tax, have been placed on maintain till additional steerage is issued.

Among the excellent points with the BMT are so daunting it’s at present unclear the tax could be salvaged as a viable income raiser with out significantly growing compliance prices and taxpayer uncertainty. To the extent the BMT is applied, there isn’t a purpose to suppose it might guarantee a minimal stage of taxation because it permits tax credit and different tax preferences. As an alternative, no matter income it raises would arbitrarily penalize sure corporations, reminiscent of these with previous losses and international earnings.[94] Accountants have warned the BMT may scale back the standard of monetary info. As these and different issues turn out to be extra obvious, the case for repealing the BMT will develop. Congress ought to reduce to the chase and relieve taxpayers and the IRS from the burden of the BMT.

In distinction, the IRA’s different main purpose of addressing local weather change by massively subsidizing inexperienced vitality seems to achieve success, no less than as indicated by the exploding price of related tax credit. Whereas many elements have contributed to this, together with different authorities insurance policies pushing within the route of a greener financial system, it can’t be denied that the credit have spurred a gold rush in direction of EVs and different inexperienced applied sciences. However, because the budgetary price of the subsidies has grown to greater than double the unique estimates, bigger budgetary disfunction and escalating deficits have adopted, main Fitch Scores to downgrade U.S. debt.[95] Because of this, Congress ought to think about controlling the fee, both by capping the credit or repealing them. Lawmakers have at their disposal extra fiscally accountable insurance policies to handle considerations about local weather change in a broad, market-based means, reminiscent of a carbon tax.

Reflecting the regulation’s rising fiscal price, the IRA might be stimulative to the financial system on internet, no less than within the short-term, till the BMT and buyback tax are totally applied, and earlier than drug worth controls current a considerable drag on drug innovation. By most accounts, the financial system in 2022 was not in want of stimulus, however slightly was extraordinarily overheated, main the Federal Reserve to boost rates of interest on the quickest tempo for the reason that Eighties. That is but another excuse to trim the IRA’s stimulative impact, notably the inexperienced vitality credit, in order that it doesn’t additional add to inflation.

In the end, the extra lawmakers simplify the tax code in fiscally accountable methods, as beneficial right here, the extra they’ll scale back inflationary pressures and enhance tax administration, the taxpayer expertise, and compliance. Whereas early indicators point out the IRA’s enhance to the IRS funds has improved customer support, which is required, the IRS can not fairly be anticipated to implement and correctly implement a brand new difficult tax on ebook revenue and 22 difficult tax credit on prime of an already overly difficult tax code, even with an expanded funds.[96] The trail to bettering the funds course of and budgetary outcomes is thru simplification.

Keep knowledgeable on the tax insurance policies impacting you.

Subscribe to get insights from our trusted consultants delivered straight to your inbox.

References

[1] Alex Durante et al., “Particulars and Evaluation of the Inflation Discount Act Tax Provisions,” Tax Basis, Aug. 12, 2022, https://taxfoundation.org/inflation-reduction-act/.

[2] See Appendix for abstract of IRS and Treasury Division steerage thus far for the ebook minimal tax, buyback tax, and inexperienced vitality tax credit.

[3] The most important provisions lined on this evaluation are the ebook minimal tax, the buyback tax, the excise tax on drug corporations, the inexperienced vitality credit, and the IRS funding enhance. The IRA contains different insurance policies not lined right here, together with an extension of the Premium Tax Credit that had been expanded within the American Rescue Plan and an extension of loss limitations for pass-through companies. See Alex Durante et al., “Particulars and Evaluation of the Inflation Discount Act Tax Provisions,” Tax Basis, Aug. 12, 2022, https://taxfoundation.org/inflation-reduction-act/.

[4] IRS, “Treasury, IRS Problem Interim Steering on New Company Various Minimal Tax,” Dec. 27, 2022, https://www.irs.gov/newsroom/treasury-irs-issue-interim-guidance-on-new-corporate-alternative-minimum-tax; IRS, “Preliminary Steering Concerning the Utility of the Company Various Minimal Tax below Sections 55, 56A, and 59 of the Inside Income Code,” Discover 2023-7, Dec. 27, 2022, https://www.irs.gov/pub/irs-drop/n-23-07.pdf; Monisha C. Santamaria, Sarah Staudenraus, Nick Tricarichi, Daniel Winnick, and Jessica Teng, “CAMTyland Adventures, Half 1: How one can Play the Recreation – Company Various Minimal Tax Fundamentals,” Tax Notes, Jul. 24, 2023, https://www.taxnotes.com/tax-notes-federal/corporate-alternative-minimum-tax/camtyland-adventures-part-i-how-play-game-corporate-alternative-minimum-tax-basics/2023/07/24/7gzqf#7gzqf-0000021; Monisha C. Santamaria, Sarah Staudenraus, Nick Tricarichi, Daniel Winnick, and Jessica Teng, “CAMTyland Adventures, Half II: ‘Proper-Sizing’ within the Licorice Lagoon,” Tax Notes, Jul. 31, 2023, https://www.taxnotes.com/tax-notes-federal/corporate-alternative-minimum-tax/camtyland-adventures-part-ii-right-sizing-licorice-lagoon/2023/07/31/7h0nq#7h0nq-0000073.

[5] See, as an illustration: Michelle Hanlon and Jeff Hoopes, “Open Letter of Concern from 264 Accounting Teachers Concerning Together with Monetary Accounting Revenue within the Tax Base,” Nov. 5, 2021, https://tax.unc.edu/index.php/news-media/open-letter-of-concern-from-264-accounting-academics-regarding-including-financial-accounting-income-in-the-tax-base/; Michelle Hanlon and Terry Shevlin, “E book-Tax Conformity for Company Revenue: An Introduction to the Points,” Tax Coverage and the Economic system 19 (September 2005), https://www.journals.uchicago.edu/doi/pdf/10.1086/tpe.19.20061897; Garrett Watson and William McBride, “Evaluating Proposals to Improve the Company Tax Price and Levy a Minimal Tax on Company E book Revenue,” Tax Basis, Feb. 24, 2021, https://taxfoundation.org/biden-corporate-income-tax-rate/; Alex Muresianu and Erica York, “It Would Be a Mistake to Resurrect the Company Various Minimal Tax,” Tax Basis, Aug. 4, 2022, https://taxfoundation.org/corporate-alternative-minimum-tax/; Cody Kallen, William McBride, and Garrett Watson, “Minimal E book Tax: Flawed Income Supply, Penalizes Professional-Progress Value Restoration,” Tax Basis, Aug. 5, 2022, https://taxfoundation.org/inflation-reduction-act-accelerated-depreciation/; Cody Kallen and Garrett Watson, “Who Will get Hit by the Inflation Discount Act E book Minimal Tax,” Tax Basis, Aug. 12, 2022, https://taxfoundation.org/book-minimum-tax-analysis/; Kyle Pomerleau, “The Minimal E book Tax Is Not a ‘Second Finest’ Reform,” American Enterprise Institute, Dec. 24, 2021, https://www.aei.org/op-eds/the-minimum-book-tax-is-not-a-second-best-reform.

[6] Brian Faler, “’Do Your Finest’: Companies Confront Dems’ New Minimal Tax With out Steering from Treasury,” Politico, Nov. 17, 2022, https://subscriber.politicopro.com/article/2022/11/do-your-best-businesses-confront-dems-new-minimum-tax-without-guidance-from-treasury-00067885; Chandra Wallace, “IRS Counsels Endurance on Company AMT Steering,” Tax Notes, Mar. 2, 2023, https://www.taxnotes.com/tax-notes-today-federal/corporate-alternative-minimum-tax/irs-counsels-patience-corporate-amt-guidance/2023/03/02/7g07k.

[7] Tax Coverage Middle, “Elevating Income from Firms,” Could 16, 2023, https://www.taxpolicycenter.org/occasion/raising-revenue-corporations; Chandra Wallace, “Broad Exclusions from Company AMT Sought by CEO Group,” Tax Notes, Mar. 27, 2023, https://www.taxnotes.com/tax-notes-today-federal/corporate-alternative-minimum-tax/broad-exclusions-corporate-amt-sought-ceo-group/2023/03/27/7g8c8; Enterprise Roundtable, “Enterprise Roundtable Feedback in Response to Discover 2023-7, Preliminary Steering Concerning the Utility of the Company Various Minimal Tax below Sections 55, 56A and 59 of the Inside Income Code,” Mar. 22, 2023, https://www.businessroundtable.org/business-roundtable-comments-in-response-to-notice-2023-7-initial-guidance-regarding-the-application-of-the-corporate-alternative-minimum-tax-under-sections-55-56a-and-59-of-the-internal-revenue-code; Alliance for Aggressive Taxation, “Feedback on Company Various Minimal Tax Discover 2023-07,” Mar. 20, 2023, https://actontaxreform.com/media/uajlaiys/act-comments-on-camt-guidance-notice-2023-7-_20230320.pdf; U.S. Chamber of Commerce, “Preliminary Feedback on Company AMT Implementation,” Mar. 23, 2023, https://www.uschamber.com/taxes/preliminary-comments-on-corporate-amt-implementation; Tim Shaw, “CPAs Touch upon Interim Company AMT Steering,” Thomson Reuters, April 18, 2023, https://tax.thomsonreuters.com/information/cpas-comment-on-interim-corporate-amt-guidance/; AICPA, “Feedback on Discover 2023-7,” Mar. 27, 2023, https://us.aicpa.org/content material/dam/aicpa/advocacy/tax/downloadabledocuments/56175896-aicpa-comment-letter-corporate-alternative-minimum-tax-notice-2023-7.pdf.

[8] Ibid.

[9] Dhammika Dharmapala, “The Tax Elasticity of Monetary Assertion Revenue: Implications for Present Reform Proposals,” Nationwide Tax Journal 73:4 (December 2020), https://www.ntanet.org/NTJ/73/4/ntj-v73n04p1047-1064-Tax-Elasticity-of-Monetary-Assertion-Revenue.html.

[10] Michelle Hanlon and Jeff Hoopes, “Open Letter of Concern from 264 Accounting Teachers Concerning Together with Monetary Accounting Revenue within the Tax Base” Nov. 5, 2021, https://tax.unc.edu/index.php/news-media/open-letter-of-concern-from-264-accounting-academics-regarding-including-financial-accounting-income-in-the-tax-base/; Michelle Hanlon and Terry Shevlin, “E book-Tax Conformity for Company Revenue: An Introduction to the Points,” Tax Coverage and the Economic system 19 (September 2005), https://www.journals.uchicago.edu/doi/pdf/10.1086/tpe.19.20061897; Garrett Watson and William McBride, “Evaluating Proposals to Improve the Company Tax Price and Levy a Minimal Tax on Company E book Revenue,” Tax Basis, Feb. 24, 2021, https://taxfoundation.org/biden-corporate-income-tax-rate/.

[11] KPMG, “KPMG Report: Draft Types Present Perception Into Compliance Burden Imposed by New CAMT,” Aug. 3, 2023, https://kpmg.com/us/en/house/insights/2023/08/tnf-kpmg-report-draft-forms-provide-insight-into-compliance-burden-imposed-by-new-camt.html.

[12] Monisha C. Santamaria, Sarah Staudenraus, Nick Tricarichi, Daniel Winnick, and Jessica Teng, “CAMTyland Adventures, Half I: How one can Play the Recreation – Company Various Minimal Tax Fundamentals,” Tax Notes, Jul. 24, 2023, https://www.taxnotes.com/tax-notes-federal/corporate-alternative-minimum-tax/camtyland-adventures-part-i-how-play-game-corporate-alternative-minimum-tax-basics/2023/07/24/7gzqf#7gzqf-0000021; Tim Shaw, “CPAs Touch upon Interim Company AMT Steering,” Thomson Reuters, Apr. 18, 2023, https://tax.thomsonreuters.com/information/cpas-comment-on-interim-corporate-amt-guidance/; AICPA, “Feedback on Discover 2023-7,” Mar. 27, 2023, https://us.aicpa.org/content material/dam/aicpa/advocacy/tax/downloadabledocuments/56175896-aicpa-comment-letter-corporate-alternative-minimum-tax-notice-2023-7.pdf; Tax Coverage Middle, “Elevating Income from Firms,” Could 16, 2023, https://www.taxpolicycenter.org/occasion/raising-revenue-corporations.

[13] Monisha C. Santamaria, Sarah Staudenraus, Nick Tricarichi, Daniel Winnick, and Jessica Teng, “CAMTyland Adventures, Half II: ‘Proper-Sizing’ within the Licorice Lagoon,” Tax Notes, Jul. 31, 2023, https://www.taxnotes.com/tax-notes-federal/corporate-alternative-minimum-tax/camtyland-adventures-part-ii-right-sizing-licorice-lagoon/2023/07/31/7h0nq#7h0nq-0000073.

[14] Michelle Hanlon and Terry Shevlin, “E book-Tax Conformity for Company Revenue: An Introduction to the Points,” Tax Coverage and the Economic system 19 (September 2005), https://www.journals.uchicago.edu/doi/pdf/10.1086/tpe.19.20061897; Tax Coverage Middle, “Elevating Income from Firms,” Could 16, 2023, https://www.taxpolicycenter.org/occasion/raising-revenue-corporations.

[15] Chandra Wallace, “Broad Exclusions from Company AMT Sought by CEO Group,” Tax Notes, Mar. 27, 2023, https://www.taxnotes.com/tax-notes-today-federal/corporate-alternative-minimum-tax/broad-exclusions-corporate-amt-sought-ceo-group/2023/03/27/7g8c8; Andrew Velarde, “Enterprise Teams Request Company AMT CFC Double-Counting Aid,” Tax Notes, Mar. 27, 2023, https://www.taxnotes.com/tax-notes-today-federal/corporate-alternative-minimum-tax/business-groups-request-corporate-amt-cfc-double-counting-relief/2023/03/27/7g8b0; Enterprise Roundtable, “Enterprise Roundtable Feedback in Response to Discover 2023-7, Preliminary Steering Concerning the Utility of the Company Various Minimal Tax below Sections 55, 56A and 59 of the Inside Income Code“, Mar. 22, 2023, https://www.businessroundtable.org/business-roundtable-comments-in-response-to-notice-2023-7-initial-guidance-regarding-the-application-of-the-corporate-alternative-minimum-tax-under-sections-55-56a-and-59-of-the-internal-revenue-code; Alliance for Aggressive Taxation, “Feedback on Company Various Minimal Tax Discover 2023-07,” Mar. 20, 2023, https://actontaxreform.com/media/uajlaiys/act-comments-on-camt-guidance-notice-2023-7-_20230320.pdf; U.S. Chamber of Commerce, “Preliminary Feedback on Company AMT Implementation,” Mar. 23, 2023, https://www.uschamber.com/taxes/preliminary-comments-on-corporate-amt-implementation.

[16] U.S. Division of the Treasury, “Treasury Releases Data on Company Various Minimal Tax,” Feb. 17, 2023, https://house.treasury.gov/information/press-releases/jy1284; IRS, “Interim Steering Concerning Sure Insurance coverage Associated Points for the Dedication of Adjusted Monetary Assertion Revenue below Part 56A of the Inside Income Code,” Discover 2023-20, Feb. 17, 2023, https://www.irs.gov/pub/irs-drop/n-23-20.pdf.

[17] Erin Slowey, “Partnerships Wrestle With Influence of US Company Minimal Tax,” Bloomberg Tax, Oct. 4, 2022, https://information.bloombergtax.com/daily-tax-report/partnerships-struggle-with-impact-of-us-corporate-minimum-tax.

[18] Alliance for Aggressive Taxation, “Feedback on Company Various Minimal Tax Discover 2023-07,” Mar. 20, 2023, https://actontaxreform.com/media/uajlaiys/act-comments-on-camt-guidance-notice-2023-7-_20230320.pdf; Tim Shaw, “CPAs Touch upon Interim Company AMT Steering,” Thomson Reuters, Apr. 18, 2023, https://tax.thomsonreuters.com/information/cpas-comment-on-interim-corporate-amt-guidance/; AICPA, “Feedback on Discover 2023-7,” Mar. 27, 2023, https://us.aicpa.org/content material/dam/aicpa/advocacy/tax/downloadabledocuments/56175896-aicpa-comment-letter-corporate-alternative-minimum-tax-notice-2023-7.pdf.

[19] Any new reporting necessities can be on prime of burdensome new guidelines that went into pressure final yr requiring partnerships to report extra info on international revenue. See, Michael Rapoport, “IRS’s Partnership Overseas Revenue Types Draw Ire of Preparers,” Bloomberg Tax, Feb. 9, 2022, https://information.bloombergtax.com/daily-tax-report-international/irss-partnership-foreign-income-forms-draw-ire-of-preparers.

[20] Jennifer Williams-Alvarez, “New Company Minimal Tax Might Ensnare Some Corporations Over One-Time Strikes,” The Wall Avenue Journal, Mar. 30, 2023, https://www.wsj.com/articles/new-corporate-minimum-tax-could-ensnare-some-firms-over-one-time-moves-260f74df.

[21] Chandra Wallace, “Broad Exclusions from Company AMT Sought by CEO Group,” Tax Notes, Mar. 27, 2023, https://www.taxnotes.com/tax-notes-today-federal/corporate-alternative-minimum-tax/broad-exclusions-corporate-amt-sought-ceo-group/2023/03/27/7g8c8; Enterprise Roundtable, “Enterprise Roundtable Feedback in Response to Discover 2023-7, Preliminary Steering Concerning the Utility of the Company Various Minimal Tax below Sections 55, 56A and 59 of the Inside Income Code,” Mar. 22, 2023, https://www.businessroundtable.org/business-roundtable-comments-in-response-to-notice-2023-7-initial-guidance-regarding-the-application-of-the-corporate-alternative-minimum-tax-under-sections-55-56a-and-59-of-the-internal-revenue-code.

[22] Chandra Wallace, “Company AMT Remark Letters Wealthy in Element – And Disagreement,” Tax Notes, Mar. 22, 2023, https://www.taxnotes.com/tax-notes-today-federal/corporate-alternative-minimum-tax/corporate-amt-comment-letters-rich-detail-and-disagreement/2023/03/22/7g804.

[23] IRS, “IRS Grants Penalty Aid for Firms That Did Not Pay Estimated Tax Associated to the New Company Various Minimal Tax,” Jun. 7, 2023, https://www.irs.gov/newsroom/irs-grants-penalty-relief-for-corporations-that-did-not-pay-estimated-tax-related-to-the-new-corporate-alternative-minimum-tax; IRS, “Aid from Sure Additions to Tax for Company’s Underpayment of Estimated Revenue Tax below Part 6655,” Discover 2023-42, Jun. 7, 2023, https://www.irs.gov/pub/irs-drop/n-23-42.pdf.

[24] Chandra Wallace, “IRS Counsels Endurance on Company AMT Steering,” Tax Notes, Mar. 2, 2023, https://www.taxnotes.com/tax-notes-today-federal/corporate-alternative-minimum-tax/irs-counsels-patience-corporate-amt-guidance/2023/03/02/7g07k; Chandra Wallace, “Treasury Undecided on Additional Interim Steering for Company AMT,” Tax Notes, Mar. 8, 2023, https://www.taxnotes.com/tax-notes-today-federal/corporate-alternative-minimum-tax/treasury-undecided-further-interim-guidance-corporate-amt/2023/03/08/7g43q.

[25] IRS, “Preliminary Steering Concerning the Utility of the Excise Tax on Repurchases of Company Inventory Below Part 4501 of the Inside Income Code,” Discover 2023-2, https://www.irs.gov/pub/irs-drop/n-23-02.pdf

[26] Jennifer Williams-Alvarez, “U.S. Buyback Tax Might Hit Extra Overseas Corporations Than First Anticipated,” The Wall Avenue Journal, Apr. 14, 2023, https://www.wsj.com/articles/u-s-buyback-tax-could-hit-more-foreign-firms-than-first-expected-e9dedec3.

[27] IRS, “Transitional Steering with Respect to Inventory Repurchase Excise Tax,” Announcement 2023-18, https://www.irs.gov/pub/irs-drop/a-23-18.pdf.

[28] Alon Brav, John Graham, Campbell R. Harvey, and Roni Michaely, “Payout Coverage within the 21st Century,” Journal of Monetary Economics 77 (September 2005), https://www.sciencedirect.com/science/article/abs/pii/S0304405X05000528; Tax Coverage Middle, “Elevating Income from Firms,” Could 16, 2023, https://www.taxpolicycenter.org/occasion/raising-revenue-corporations.

[29] Erica York, “Tax on Inventory Buybacks a Misguided Technique to Encourage Funding,” Tax Basis, Sep. 10, 2021, https://taxfoundation.org/tax-on-stock-buybacks/.

[30] Alex Durante, “Inventory Buyback Tax Would Damage Funding and Innovation,” Tax Basis, Aug. 12, 2022, https://taxfoundation.org/inflation-reduction-act-stock-buybacks/.

[31] Alex Muresianu, “Breaking Down the Inflation Discount Act’s Inexperienced Power Credit,” Tax Basis, Sep. 14, 2022, https://taxfoundation.org/inflation-reduction-act-green-energy-tax-credits/.

[32] John Podesta, “Constructing a Clear Power Economic system: A Guidebook to the Inflation Discount Act’s Investments in Clear Power and Local weather Motion,” CleanEnergy.gov, January 2023, https://www.whitehouse.gov/wp-content/uploads/2022/12/Inflation-Discount-Act-Guidebook.pdf.

[33] EPA, “Sources of Greenhouse Gasoline Emissions,” U.S. Environmental Safety Company, https://www.epa.gov/ghgemissions/sources-greenhouse-gas-emissions.

[34] Kyle Pomerleau, “Testimony: Non permanent Coverage within the Federal Tax Code,” Tax Basis, Mar. 13, 2019, https://taxfoundation.org/testimony-temporary-tax-policy/.

[35] Inside Income Service, “Prevailing Wage and Apprenticeship Preliminary Steering Below Part 45(b)(6)(B)(ii) and Different Considerably Related Provisions,” Discover 2022-61, Nov. 30, 2022, https://www.federalregister.gov/paperwork/2022/11/30/2022-26108/prevailing-wage-and-apprenticeship-initial-guidance-under-section-45b6bii-and-other-substantially.

[36] Inside Income Service, “Preliminary Steering Establishing Program to Allocate Environmental Justice Photo voltaic and Wind Capability Limitation Below Part 48(e),” Discover 2023-17, Feb. 13, 2023, https://www.irs.gov/pub/irs-drop/n-23-17.pdf; Inside Income Service, “Power Neighborhood Bonus Credit score Quantities below the Inflation Discount Act,” Discover 2023-29, Apr. 4, 2023, https://www.irs.gov/pub/irs-drop/n-23-29.pdf; Inside Income Service, “Power Neighborhood Bonus Credit score Quantities Below the Inflation Discount Act of 2022,” Discover 2023-45, Jun. 15, 2023, https://www.irs.gov/pub/irs-drop/n-23-45.pdf.

[37] Inside Income Service, “Home Content material Bonus Credit score Steering Below Part 45, 45Y, 48, and 48E,” Discover 2023-38, Could 12, 2023, https://www.irs.gov/pub/irs-drop/n-23-38.pdf.

[38] Inside Income Service, “Elective Pay and Transferability Steadily Requested Questions: Overview,” Jun. 14, 2023, https://www.irs.gov/credits-deductions/elective-pay-and-transferability-frequently-asked-questions-overview.

[39] Scott Hodge, “’Monetizing’ Clear Power Tax Credit Creates a Sham Marketplace for Dangerous Coverage,” Tax Basis, Jul. 18, 2023, https://taxfoundation.org/irs-clean-energy-tax-credits/.

[40] Inside Income Service, “Sustainable Aviation Gas Credit score; Registration; Certificates; Request for Public Feedback,” Discover 2023-06, Dec. 19, 2022, https://www.irs.gov/pub/irs-drop/n-23-06.pdf.

[41] Natalie Houghtalen, “Hydrogen 101,” ClearPath, Feb. 11, 2021, https://clearpath.org/tech-101/hydrogen-101/.

[42] Inside Income Service, “IRS Points Steering and Updates Steadily Requested Questions Associated to the New Clear Car Vital Mineral and Battery Parts,” Apr. 17, 2023, https://www.federalregister.gov/paperwork/2023/04/17/2023-06822/section-30d-new-clean-vehicle-credit.

[43] Chad Brown, “How america Solved South Korea’s Issues with Electrical Car Subsidies Below the Inflation Discount Act,” Peterson Institute for Worldwide Economics Working Paper 23-6, July 2023, https://www.piie.com/publications/working-papers/how-united-states-solved-south-koreas-problems-electric-vehicle.

[44] Ibid; see additionally Inside Income Service, “Part 30D New Clear Car Credit score,” Mar. 31, 2023, https://www.federalregister.gov/paperwork/2023/04/17/2023-06822/section-30d-new-clean-vehicle-credit.

[45] Barbara Moens, Steven Overly, and Sarah Anne Aarup, “U.S. Pumps the Brakes on EU Clear Automotive Deal,” Politico, Could 22, 2023, https://www.politico.com/information/2023/05/21/us-eu-clean-car-deal-00098092.

[46] Inside Income Service, “Submission of Data to IRS by Certified Producers of Clear Autos, Beforehand-Owned Clear Autos, and Business Clear Autos; Submission of Data to IRS by Sellers of Clear Autos and Beforehand-Owned Clear Autos,” Income Process 2022-42, Dec. 12, 2022, https://www.irs.gov/pub/irs-drop/rp-22-42.pdf; see additionally Inside Income Service, “Sure Definitions of Phrases in Part 30D Clear Car Credit score,” Discover 2023-1, Dec. 29, 2022, https://www.irs.gov/pub/irs-drop/n-23-01.pdf; Inside Income Service, “Sure Definitions of Phrases in Part 30D Clear Car Credit score,” Discover 2023-16, Feb. 3, 2023, https://www.irs.gov/pub/irs-drop/n-23-16.pdf.

[47] Inside Income Service, “Part 45W Business Clear Autos and Incremental Value for 2023,” Discover 2023-9, Dec. 29, 2022, https://www.irs.gov/pub/irs-drop/n-23-09.pdf; see additionally Inside Income Service, “Sure Definitions of Phrases in Part 30D Clear Car Credit score.”

[48] Inside Income Service, “Steadily Requested Questions About Power Environment friendly Residence Enhancements and Nonbusiness Power Property Credit,” Reality Sheet 2022-40, Dec. 22, 2022, https://www.irs.gov/pub/taxpros/fs-2022-40.pdf.

[49] Ibid.

[50] Brendan McDermott, “Residential Power Tax Credit: Adjustments in 2023,” Congressional Analysis Service, Nov. 21, 2022, https://crsreports.congress.gov/product/pdf/IN/IN12051.

[51] Dave Sobochan and Mike McGivney, “15 Takeaways from the Inflation Discount Act’s Clear Power Tax Incentives,” Cohen & Co., Aug. 26, 2022, https://www.cohencpa.com/knowledge-center/insights/august-2022/15-takeaways-from-the-inflation-reduction-act-clean-energy-tax-incentives.

[52] Alex Muresianu, “How Expensing for Capital Funding Can Speed up the Transition to a Cleaner Economic system,” Tax Basis, Jan. 12, 2021, https://taxfoundation.org/analysis/all/federal/energy-efficiency-climate-change-tax-policy/.

[53] Inside Income Service, “Prevailing Wage and Apprenticeship Preliminary Steering Below Part 45(b)(6)(B)(ii) and Different Considerably Related Provisions.”

[54] Clear Air Activity Power, “Carbon Seize and the Inflation Discount Act,” Aug. 19, 2022, https://cdn.catf.us/wp-content/uploads/2023/02/16093309/ira-carbon-capture-fact-sheet.pdf.

[55] Barbara S. de Marigny, “Agency Notes Ambiguity in Carbon Oxide Sequestration Credit score Provisions,” Baker Botts LLP, Jun. 8, 2023, https://www.taxnotes.com/analysis/federal/other-documents/irs-tax-correspondence/firm-notes-ambiguity-in-carbon-oxide-sequestration-credit-provisions/7h1c4?spotlight=Depercent20Marignypercent20Barbara#7h1c4-0000009.

[56] Inside Income Service, “Preliminary Steering Establishing Qualifying Superior Power Challenge Credit score Allocation Program Below Part 48(e),” Discover 2023-18, Feb. 13, 2023, https://www.irs.gov/pub/irs-drop/n-23-18.pdf.

[57] Diana DiGangi, “Treasury Points Additional Steering for IRA’s $10B Tax Credit score Incentivizing Clear Power Manufacturing,” Utility Dive, Jun. 1, 2023, https://www.utilitydive.com/information/ira-clean-energy-manufacturing-tax-credit-ten-billion-irs-guidance/651807/.

[58] Ibid; Inside Income Service, “Further Steering for the Qualifying Superior Power Challenge Credit score Allocation Program below Part 48C(e),” Discover 2023-44, Could 31, 2023, https://www.irs.gov/pub/irs-drop/n-23-44.pdf;

[59] Worldwide Power Company, “Inflation Discount Act 2022: Sec. 13502 Superior Manufacturing Manufacturing Credit score,” Could 24, 2023, https://www.iea.org/insurance policies/16282-inflation-reduction-act-2022-sec-13502-advanced-manufacturing-production-credit.

[60] Inside Income Service, “Treasury, IRS Problem Steering for the Superior Manufacturing Funding Credit score,” Jun. 14, 2023, https://www.irs.gov/newsroom/treasury-irs-issue-guidance-for-the-advanced-manufacturing-investment-credit.

[61] William McBride and Daniel Bunn, “Repealing Inflation Discount Act’s Power Credit Would Elevate $663 Billion, JCT Tasks,” Tax Basis, Jun. 7, 2023, https://taxfoundation.org/inflation-reduction-act-green-energy-tax-credits-analysis/.

[62] The White Home, “Nationwide Local weather Activity Power,” accessed Aug. 2, 2023, https://www.whitehouse.gov/local weather/.

[63] Environmental Safety Company, “Multi-Pollutant Emissions Requirements for Mannequin Years 2027 and Later Mild-Obligation and Medium-Obligation Autos,” April 2023, https://www.epa.gov/system/recordsdata/paperwork/2023-04/420d23003.pdf; Division of Transportation, “Company Common Gas Economic system,” accessed Aug. 2, 2023, https://www.nhtsa.gov/laws-regulations/corporate-average-fuel-economy.

[64] Ibid., see additionally Martin Sullivan, “EPA Estimates Its Regs Would Value Treasury A whole bunch of Billions,” Tax Notes, Jun. 20, 2023, https://www.taxnotes.com/tax-notes-today-federal/energy-taxation/epa-estimates-its-regs-would-cost-treasury-hundreds-billions/2023/06/20/7gwb0.

[65] Penn-Wharton Finances Mannequin, “Replace: Budgetary Value of Local weather and Power Provisions within the Inflation Discount Act,” Apr. 27, 2023, https://budgetmodel.wharton.upenn.edu/estimates/2023/4/27/update-cost-climate-and-energy-inflation-reduction-act; Goldman Sachs, “Carbonomics: The Third American Power Revolution,” Mar. 22, 2023.

[66] John Bistline, Neil Mehrotra, and Catherine Wolfram, “Financial Implications of the Local weather Provisions of the Inflation Discount Act,” Brookings Papers on Financial Exercise, Mar. 30, 2023, https://www.brookings.edu/wp-content/uploads/2023/03/BPEA_Spring2023_Bistline-et-al_unembargoedUpdated.pdf; see additionally Christine McDaniel, “The Value of Battery Manufacturing Tax Credit Offered in The IRA,” Forbes, Feb. 1, 2023, https://www.forbes.com/websites/christinemcdaniel/2023/02/01/the-cost-of-battery-production-tax-credits-provided-in-the-ira/?sh=6a32399679ef; Christine McDaniel, “The Value of Wind Manufacturing Tax Credit Offered within the IRA,” Forbes, Mar. 8, 2023, https://www.forbes.com/websites/christinemcdaniel/2023/03/08/the-costs-of-wind-production-tax-credits-provided-in-the-ira/?sh=7ba0259d5ff7.

[67] Joseph Politano, “America’s Industrial Transition: U.S. Manufacturing is Slowing-Excluding the Report Spending on Semiconductor Fabricators and Tech Manufacturing Crops,” Apricitas Economics, Apr. 26, 2023, https://www.apricitas.io/p/americas-industrial-transition; Bureau of Financial Evaluation, “Gross Home Product: Second Estimate,” Jul. 27, 2023, https://www.bea.gov/websites/default/recordsdata/2023-07/gdp2q23_adv.pdf.

[68] John Bistline, Neil Mehrotra, and Catherine Wolfram, “Financial Implications of the Local weather Provisions of the Inflation Discount Act,” Brookings Papers on Financial Exercise, Mar. 30, 2023, https://www.brookings.edu/wp-content/uploads/2023/03/BPEA_Spring2023_Bistline-et-al_unembargoedUpdated.pdf.

[69] https://www.pwc.com/us/en/providers/tax/library/inflation-reduction-act-considerations-for-pharma-companies.html.

[70] Congressional Finances Workplace, “Re: Results of Drug Value Negotiation Stemming From Title 1 of H.R. 3, the Decrease Drug Prices Now Act of 2019, on Spending and Revenues Associated to Half D of Medicare,” Oct. 11, 2019, https://www.cbo.gov/system/recordsdata/2019-10/hr3ltr.pdf.

[71] Erica York, “Paying for Reconciliation Invoice with “Well being Care Financial savings” Threatens Medical Innovation,” Tax Basis, Aug. 25, 2021, https://taxfoundation.org/medicare-part-d-hr3-lower-drug-prices/.

[72] See abstract in Erica York,” Inflation Discount Act’s Value Controls Are Deterring New Drug Growth,” Tax Basis, Apr. 26, 2023, https://taxfoundation.org/inflation-reduction-act-medicare-prescription-drug-price-controls/.

[73] Facilities for Medicare & Medicaid Providers, “Medicare Drug Value Negotiation Program: Preliminary Memorandum, Implementation of Sections 1191 – 1198 of the Social Safety Act for Preliminary Value Applicability Yr 2026, and Solicitation of Feedback,” Mar. 15, 2023, https://www.cms.gov/recordsdata/doc/medicare-drug-price-negotiation-program-initial-guidance.pdf.

[74] For instance, see the approaches described in Alex Durante, “Tackling America’s Debt and Deficit Disaster Requires Social Safety and Medicare Reform,” Tax Basis, Could 23, 2023, https://taxfoundation.org/medicare-social-security-reform-us-debt-deficits/.

[75] Daniel Werfel, “Inside Income Service Inflation Discount Act Strategic Working Plan, FY2023 – 2031,” Inside Income Service, Apr. 5, 2023, https://www.irs.gov/pub/irs-pdf/p3744.pdf.

[76] Division of the Treasury, “How a Remodeled IRS Will Enhance Tax Equity,” Aug. 15, 2022, https://house.treasury.gov/system/recordsdata/136/TaxFairnessSOPOnePager.pdf.

[77] Alex Muresianu, “How one can Suppose About IRS Enforcement Provisions within the Inflation Discount Act,” Tax Basis, Aug. 17, 2022, https://taxfoundation.org/inflation-reduction-act-irs-funding/.