[ad_1]

On 12 September, the European Fee launched a proposal referred to as “Enterprise in Europe: Framework for Revenue TaxA tax is a compulsory fee or cost collected by native, state, and nationwide governments from people or companies to cowl the prices of basic authorities providers, items, and actions.

ation” (BEFIT) and two related proposals on switch pricing and a Head of Workplace tax system.

BEFIT replaces the Fee’s earlier proposals aimed toward creating a typical company tax baseThe tax base is the whole quantity of earnings, property, property, consumption, transactions, or different financial exercise topic to taxation by a tax authority. A slim tax base is non-neutral and inefficient. A broad tax base reduces tax administration prices and permits extra income to be raised at decrease charges.

referred to as CCTB (frequent company tax base) and CCCTB (frequent consolidated company tax base). Whereas the brand new proposal intends to cut back cross-border frictions for firms working in a number of Member States, BEFIT depends on monetary accounting guidelines (relatively than conventional tax guidelines) and should find yourself including one other layer of complexity for enterprise.

BEFIT’s Scope

The BEFIT proposal is designed to construct on the OECD’s world tax deal. It contains necessary obligations for sure firms and voluntary participation for others.

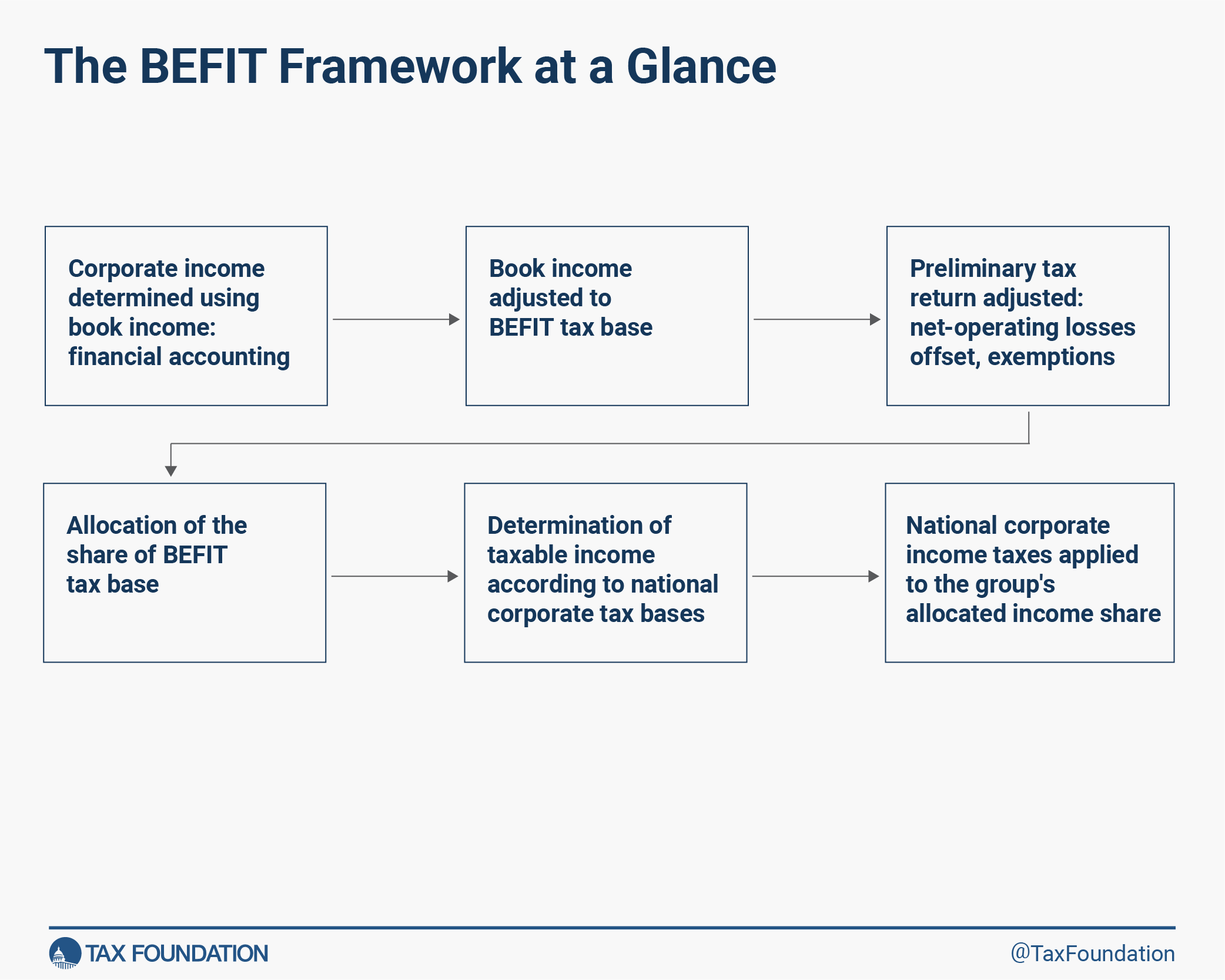

The necessary scope of the proposal contains multinational firms with world consolidated revenues above EUR 750 million—the identical thresholds in Pillar Two. Extra standards apply for enterprises with an EU possession share under the 75 % threshold. Related firms—referred to as BEFIT teams—must file a single preliminary tax return primarily based on a fictitious frequent tax base for all their EU-based subsidiaries (BEFIT members).

The preliminary tax returns would then be used to evaluate compliance dangers with switch pricing guidelines and allocate shares of the frequent company tax base to EU Member States to which they apply their very own nationwide company earnings taxA company earnings tax (CIT) is levied by federal and state governments on enterprise earnings. Many firms usually are not topic to the CIT as a result of they’re taxed as pass-through companies, with earnings reportable below the particular person earnings tax.

programs. In line with the present proposal, Member States would wish to implement the brand new guidelines by 1 January 2028, with utility to BEFIT teams beginning 1 July 2028.

Calculating the Base and Allocation Guidelines

The proposed BEFIT framework strikes away from a conventional company tax base to at least one that depends on monetary accounting. Whereas this pattern just isn’t new—it has been utilized in Pillars One and Two, in addition to the USA’ company various minimal tax (CAMT)—it may be difficult, advanced, and inaccurate. Simply because you might have a measure of “earnings” doesn’t imply that it’s going to make a very good tax base. A typical definition doesn’t essentially enhance upon the approaches on the Member State degree.

Company earnings is decided utilizing the guide earningsE-book earnings is the quantity of earnings companies publicly report on their monetary statements to shareholders. This measure is helpful for assessing the monetary well being of a enterprise however usually doesn’t mirror financial actuality and may end up in a agency showing worthwhile whereas paying little or no earnings tax.

of the father or mother entity and adjusting the ensuing monetary statements based on the BEFIT tax base guidelines.

The monetary accounts statements should observe European Union regulation, utilizing both the nationwide typically accepted accounting ideas (GAAP) of one of many Member States or the worldwide financing reporting requirements (IFRS). Monetary statements produced below these requirements mirror guide earnings, a measure utilized by firms to report their earnings and bills to shareholders and collectors to point their monetary well being—a objective distinct from figuring out firms’ tax legal responsibility.

Offsetting Web Working Losses and Exempting Sure WithholdingWithholding is the earnings an employer takes out of an worker’s paycheck and remits to the federal, state, and/or native authorities. It’s calculated primarily based on the quantity of earnings earned, the taxpayer’s submitting standing, the variety of allowances claimed, and any further quantity of the worker requests.

Taxes

E-book earnings is then adjusted in accordance with the foundations governing the BEFIT tax base for depreciationDepreciation is a measurement of the “helpful life” of a enterprise asset, similar to equipment or a manufacturing unit, to find out the multiyear interval over which the price of that asset may be deducted from taxable earnings. As an alternative of permitting companies to deduct the price of investments instantly (i.e., full expensing), depreciation requires deductions to be taken over time, decreasing their worth and discouraging funding.

, stock remedy, loss carryover provisions, and different adjustments to reach on the company earnings measure for the preliminary BEFIT tax return (notably, not at all times aligned with Pillar Two). For the preliminary tax return, BEFIT teams can offset web working losses between their members in the identical yr and are additionally exempted from withholding taxes on transactions between group members. The latter step appears to be one the place substantive cross-border frictions are eradicated, smoothing their enterprise operations throughout Europe.

However the framework doesn’t cease there. BEFIT teams’ taxable earningsTaxable earnings is the quantity of earnings topic to tax, after deductions and exemptions. For each people and companies, taxable earnings differs from—and is lower than—gross earnings.

is then allotted to the Member States utilizing the common share of the BEFIT tax base originating of their jurisdiction over the previous three fiscal years. For jurisdictions utilizing distributed revenue tax programs, like Estonia and Latvia, an tailored system is used to allocate nationwide shares considering that in these programs; company earnings are solely taxed upon distribution to shareholders.

After the allocation of particular person Member States’ shares of the BEFIT tax base, nationwide company earnings taxes are utilized to the group’s allotted earnings share to every jurisdiction. The principles governing the nationwide company earnings tax will often differ from these of the BEFIT tax base. Subsequently, evidently group members will nonetheless should individually decide their taxable earnings based on completely different nationwide guidelines for all related jurisdictions.

One-Cease-Store or One-Extra-Cease?

Whereas the proposal speaks of a “one-stop-shop” for EU tax returns, the fact could look extra like “one-more-stop.” As an alternative of submitting their nationwide tax returns below a single algorithm, a BEFIT group could should file one preliminary tax return to calculate the BEFIT tax base allotted to Member States, along with all their nationwide tax returns figuring out their closing tax legal responsibility. This exerts strain on Member States to align their nationwide tax legal guidelines with the BEFIT tax base to keep away from duplicative compliance prices. Because of this the chart above solely exhibits the BEFIT tax base for firms, not together with what they must do along with submitting their nationwide tax returns.

This introduces a further layer of complexity for firms. Past nationwide company taxation and compliance with the 15 % minimal tax established by Pillar Two, firms can even have to fret in regards to the new BEFIT tax base. Under is a restricted abstract evaluating the GloBE and BEFIT tax bases.

Switch Pricing Benchmark

The preliminary tax returns filed for BEFIT teams enter a screening course of for switch pricing compliance threat in “low-risk” manufacturing and distribution actions, which aren’t linked to holding of mental property rights.

The proposal introduces a “site visitors gentle” system that evaluates company earnings from BEFIT tax returns in opposition to a revenue benchmark—consultant for impartial entities in these sectors working within the EU—and classifies the transactions of a BEFIT group inside a low-, medium-, or high-risk zone.

If a bunch’s company earnings lie significantly under the benchmark, indicating revenue shiftingRevenue shifting is when multinational firms cut back their tax burden by transferring the placement of their earnings from high-tax nations to low-tax jurisdictions and tax havens.

, the “site visitors gentle” system would flag the corporate for the “high-risk” class, signalling to nationwide auditA tax audit is when the Inner Income Service (IRS) conducts a proper investigation of economic info to confirm a person or company has precisely reported and paid their taxes. Choice may be at random, or as a consequence of uncommon deductions or earnings reported on a tax return.

ing authorities to take a more in-depth look. Facilitating stronger compliance with switch pricing insurance policies whereas dropping withholding taxes on intra-group transactions seems to be a key motivation of the BEFIT proposal.

For the reason that revenue measure below BEFIT differs from firms’ taxable earnings, an apples-to-apples comparability would require additionally calculating the equal revenue measure of impartial entities based on BEFIT guidelines to find out the revenue benchmark.

Questions for the European Fee

BEFIT doesn’t seem to meaningfully cut back the complexity of company taxation in Europe. Whereas the proposal would remove some cross-border frictions inside the European Union, it might nonetheless create a further layer of complexity for companies working below the framework as a result of it has a special tax base than Pillar Two. As an alternative of submitting their nationwide tax returns below a single algorithm, a BEFIT group could should file one preliminary tax return for the fictional BEFIT tax base, along with all their legally binding nationwide tax returns. Moreover, the BEFIT earnings calculation depends on monetary accounting guidelines, that are distinct from legally binding taxable earnings.

As presently written, there are basic questions the European Fee ought to reply earlier than being thought-about by the Council:

- What occurs when there’s a distinction between company tax owed below Member State guidelines and BEFIT guidelines?

- Are the capital allowanceA capital allowance is the quantity of capital funding prices, or cash directed in direction of an organization’s long-term progress, a enterprise can deduct every year from its income through depreciation. These are additionally generally known as depreciation allowances.

s and loss provisions outlined within the proposal extra aggressive than the established order? - What is going to the influence of BEFIT be on the European Union’s Personal Sources?

It will likely be troublesome for specialists to noticeably take into account the prices and advantages of the BEFIT proposal with out answering these questions. As the present mandate ends subsequent spring, it’s crucial that the Fee reply to supply these particulars in a well timed method.

Notice: This publish is a part of an upcoming BEFIT sequence that may search to reply a few of these questions, present a deeper evaluation of the proposal, and provides some European context.

Keep knowledgeable on the tax insurance policies impacting you.

Subscribe to get insights from our trusted specialists delivered straight to your inbox.

Share

[ad_2]

Supply hyperlink