[ad_1]

Key outcomes:

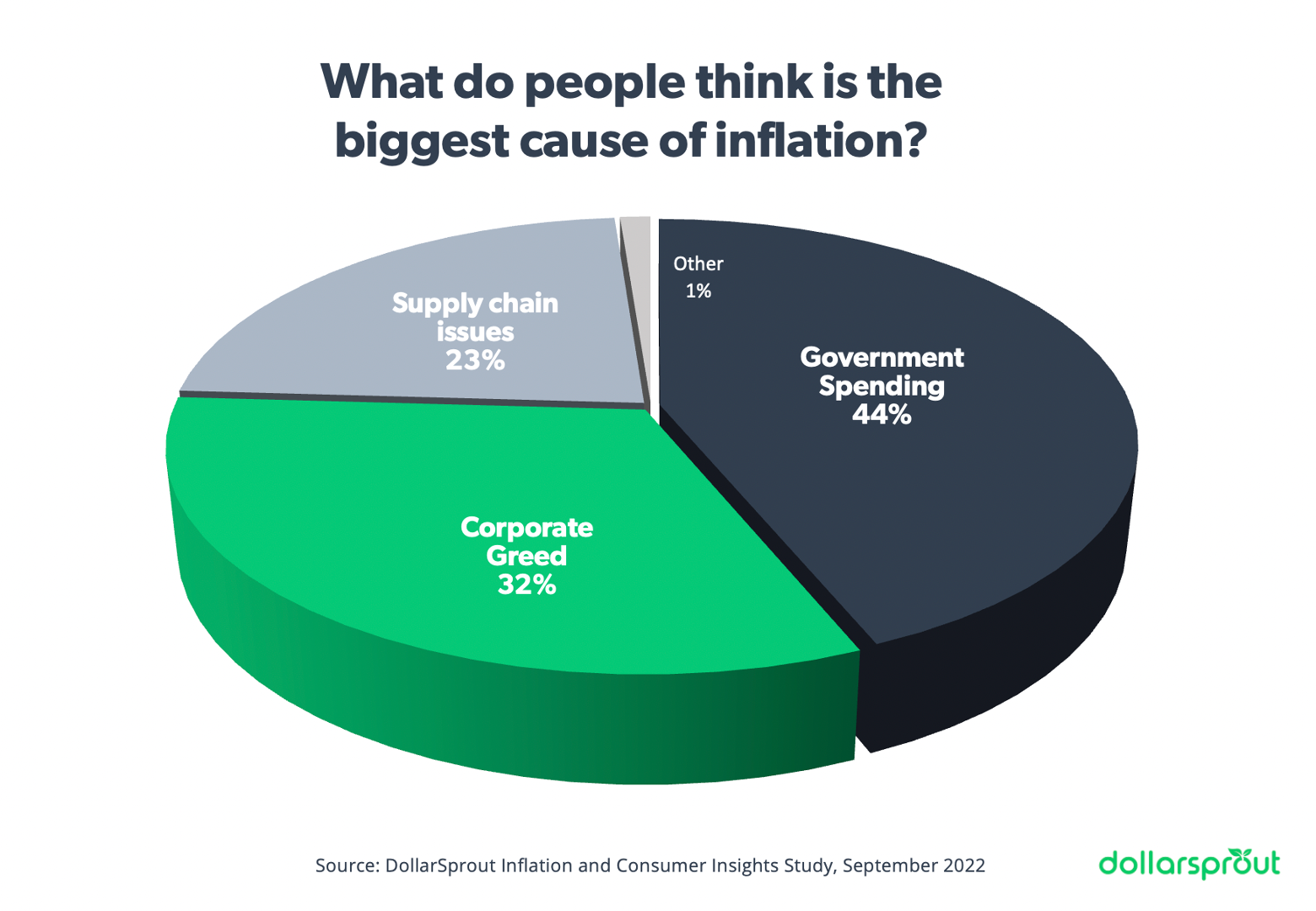

» 44% of Individuals consider that authorities spending is the principle explanation for inflation.

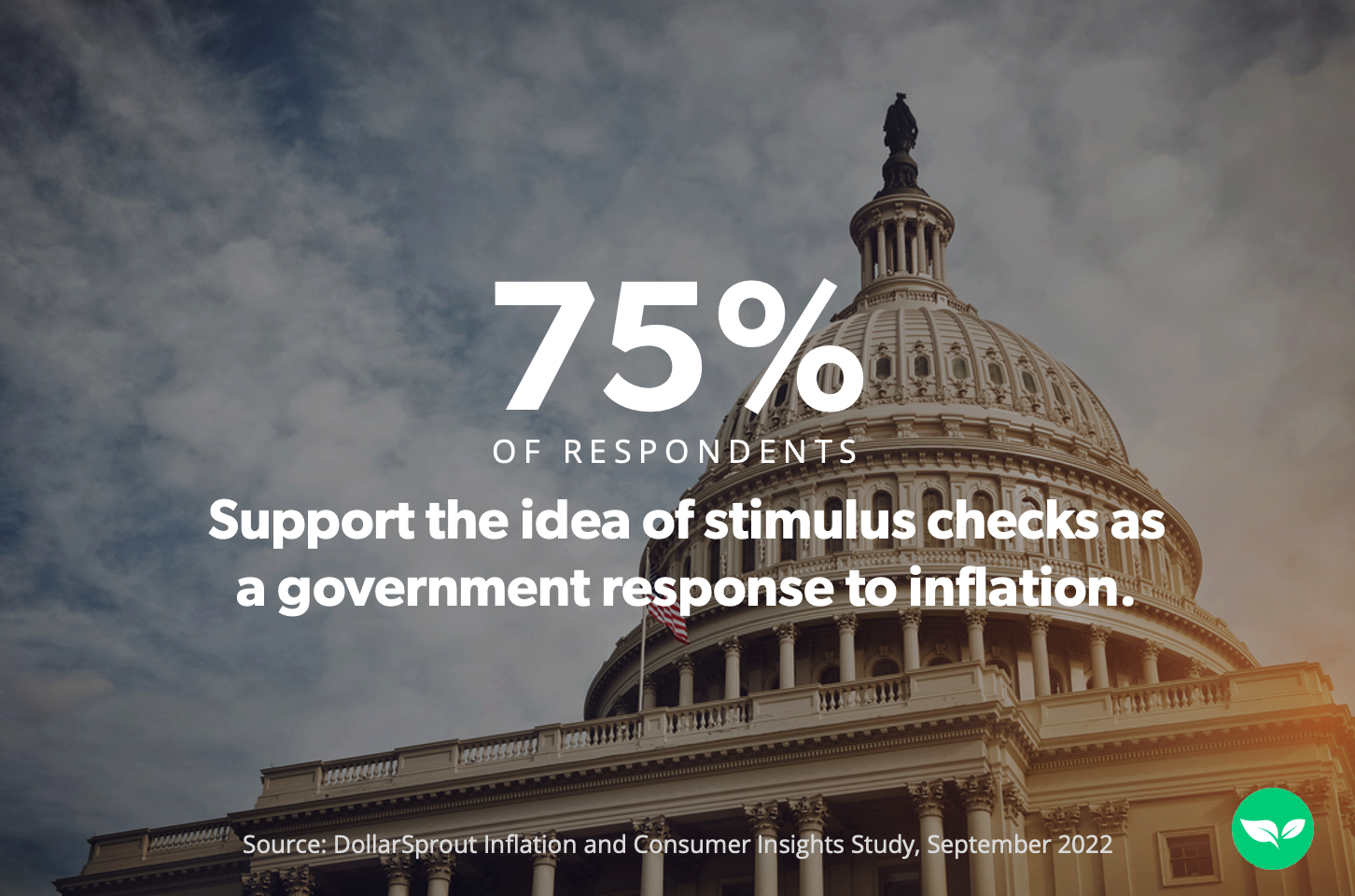

” On the similar time, 75% of Individuals favor stimulus checks as a way of preventing inflation.

» 70% of customers report shopping for generic manufacturers extra usually.

» 49% of respondents say they’re saving much less for retirement or not saving in any respect.

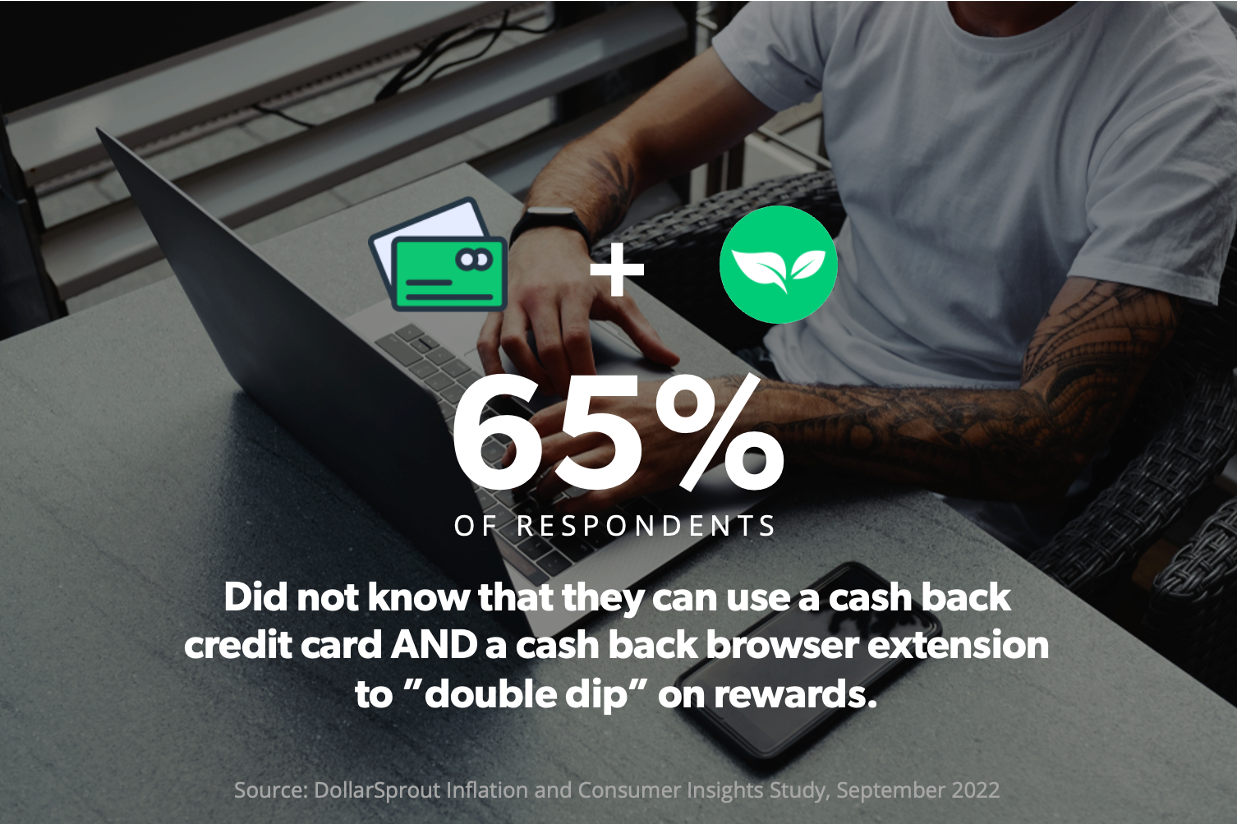

» Sixty-five% They do not know they will use a money again bank card AND a money again browser extension to “double dip” the rewards.

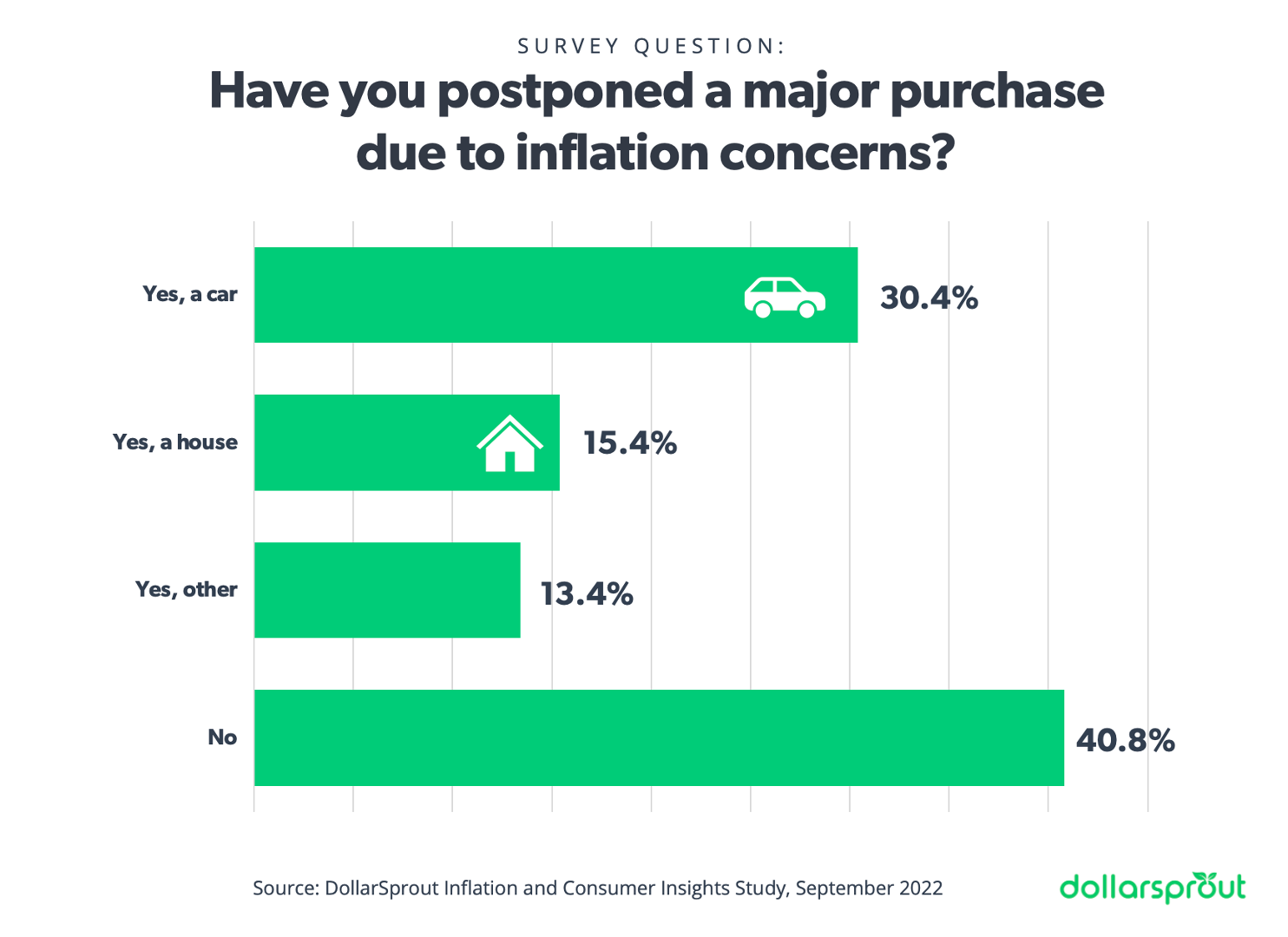

» 30% report the delay in shopping for a automotive and fifteen% have delayed shopping for a house because of inflation points.

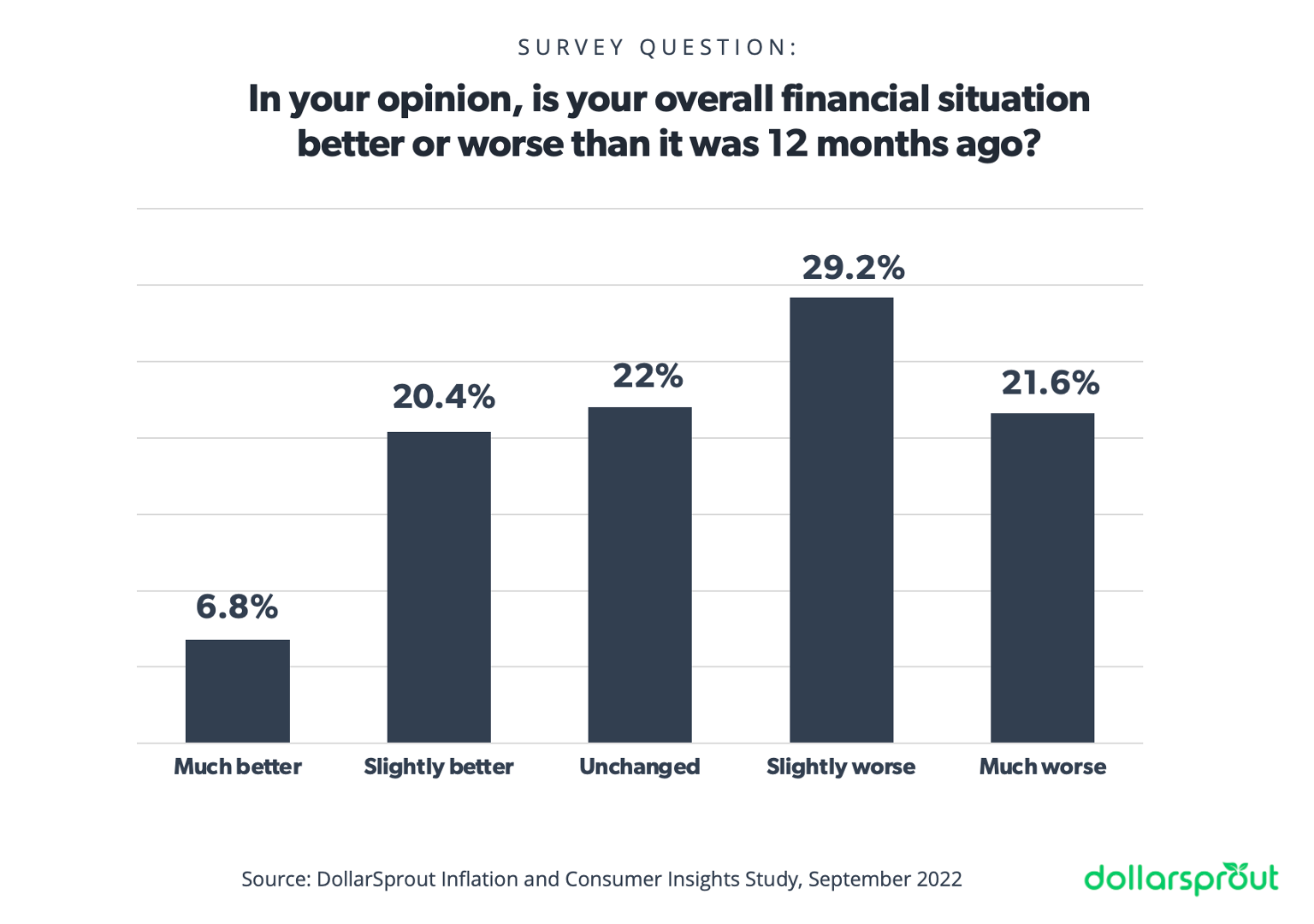

» 51% they are saying they’re in a worse monetary state of affairs than a yr in the past.

With the newest inflation figures popping out, issues should not trying excellent. Based on the newest knowledge As revealed by the US Bureau of Labor Statistics, the price of dwelling is 8.3% greater than this time final yr and nonetheless exhibits no indicators of declining. There isn’t any scarcity of opinion amongst Individuals as to who’s guilty or what’s the finest plan of action from right here.

To raised perceive how inflation impacts individuals, DollarSprout carried out a survey amongst a broad pattern of Individuals from all walks of life. Listed here are the outcomes.

Irony between trigger and answer

Whereas it is cheap to suppose that many various elements contribute to inflation, once we requested what individuals thought of bigger the trigger was that the principle reply was “public spending”.

Most shocking, although, was the response we noticed once we requested a couple of attainable answer: stimulus checks. In current months, varied states They’ve introduced that they’re issuing stimulus checks to residents.

Even if public spending is talked about as the principle explanation for inflation, 3 out of 4 respondents supported the thought of stimulus checks as a authorities response to inflation.

How are individuals adjusting to the worth improve?

When inflation considerations started to floor late final yr and early this yr, many customers have been sluggish to make adjustments. The Fed infamously claimed that inflation was “transient,” that means it might go rapidly. The truth has now begun to sink in that inflation is right here to remain in the meanwhile, and it’s now having a way more noticeable impression on customers.

The issue of inflation is extra important than simply elevating the price of eggs and bread by a number of cents. The truth is, greater than 50% of these surveyed reported that they’ve delay a serious buy because of the present inflationary surroundings.

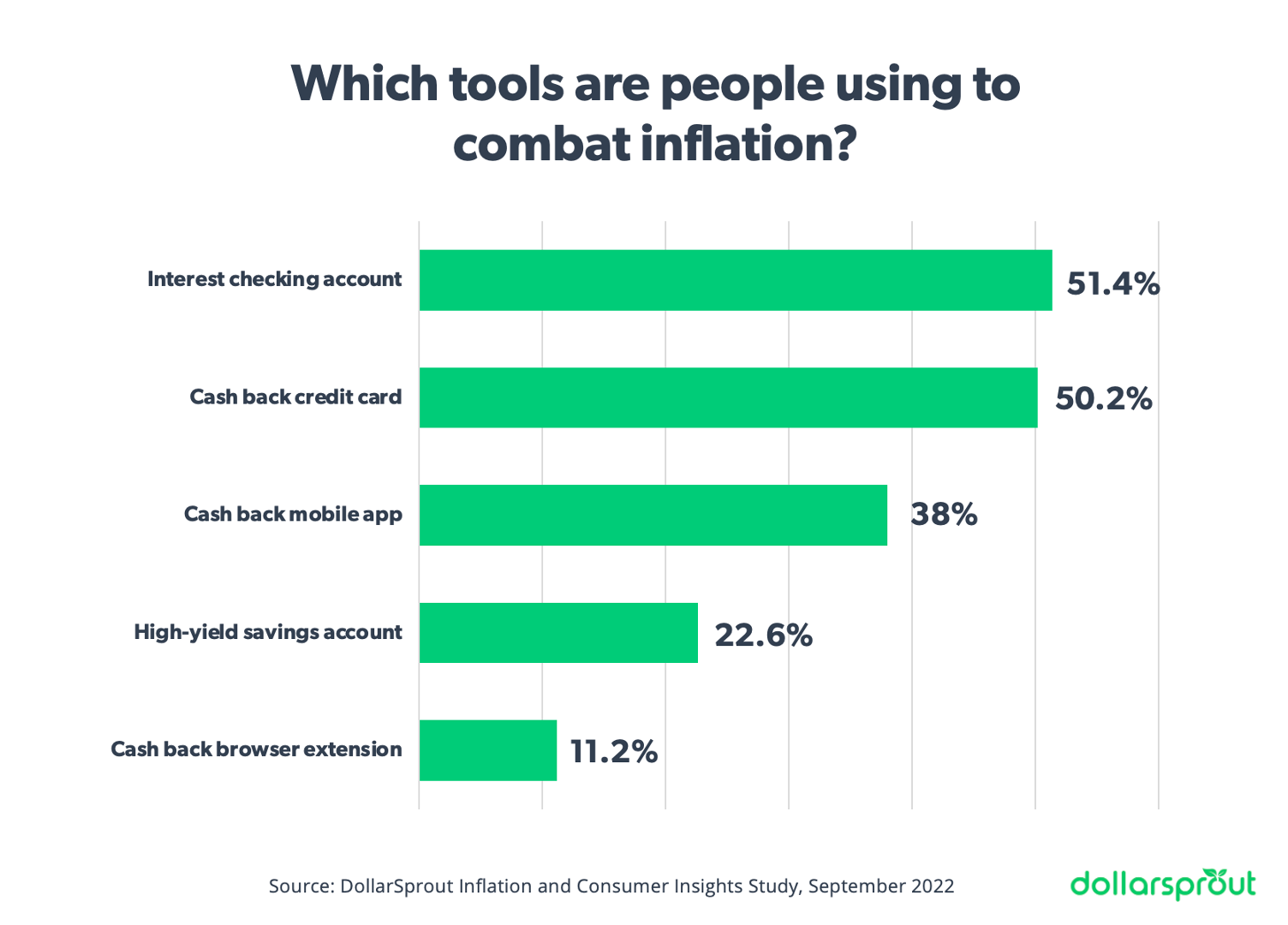

Many should not utilizing all of the instruments at their disposal

With meals, fuel and housing turning into costlier and wages not rising quick sufficient to compensate, individuals are working out of choices. Nonetheless, the info exhibits that many individuals are nonetheless underutilizing each attainable instrument at their disposal to battle inflation.

And for a way frequent money again bank cards are, it is wonderful to see that 65% of individuals did not know they will double the rewards through the use of a money again bank card and a money again cellular app or a browser extension in the identical buy. . For instance, if a Chase card presents 1.5% money again and a Chrome money again extension presents one other 2% money again at a selected retailer, the patron will get a mixed 3.5 money again % money on a single buy.

With inflation working simply over 8% on the time of this report, cash-back double-dipping is probably essentially the most important technique to battle rising prices. Getting 4% money again on one thing that prices 8% greater than final yr goes a great distance.

One other frequent blind spot amongst customers is the lively seek for coupon codes. More often than not we consider coupon codes once we see an influencer share their code on Instagram or a retailer ship a coupon code in an electronic mail, however simply since you did not see a coupon code marketed to you doesn’t suggest you have not. Do it. doesn’t exist Greater than 1 in 10 internet buyers by no means proactively seek for low cost codes, and solely barely lower than half at all times seek for them. The remainder solely “generally” ask for reductions.

Some money again extensions like Honey will routinely discover any obtainable coupon codes with out the consumer having to dig round.

Folks’s funds are trending within the improper route

To get a extra correct image of how individuals really feel about their general funds (not nearly inflation), we requested individuals in the event that they felt their state of affairs was higher or worse than 12 months in the past.

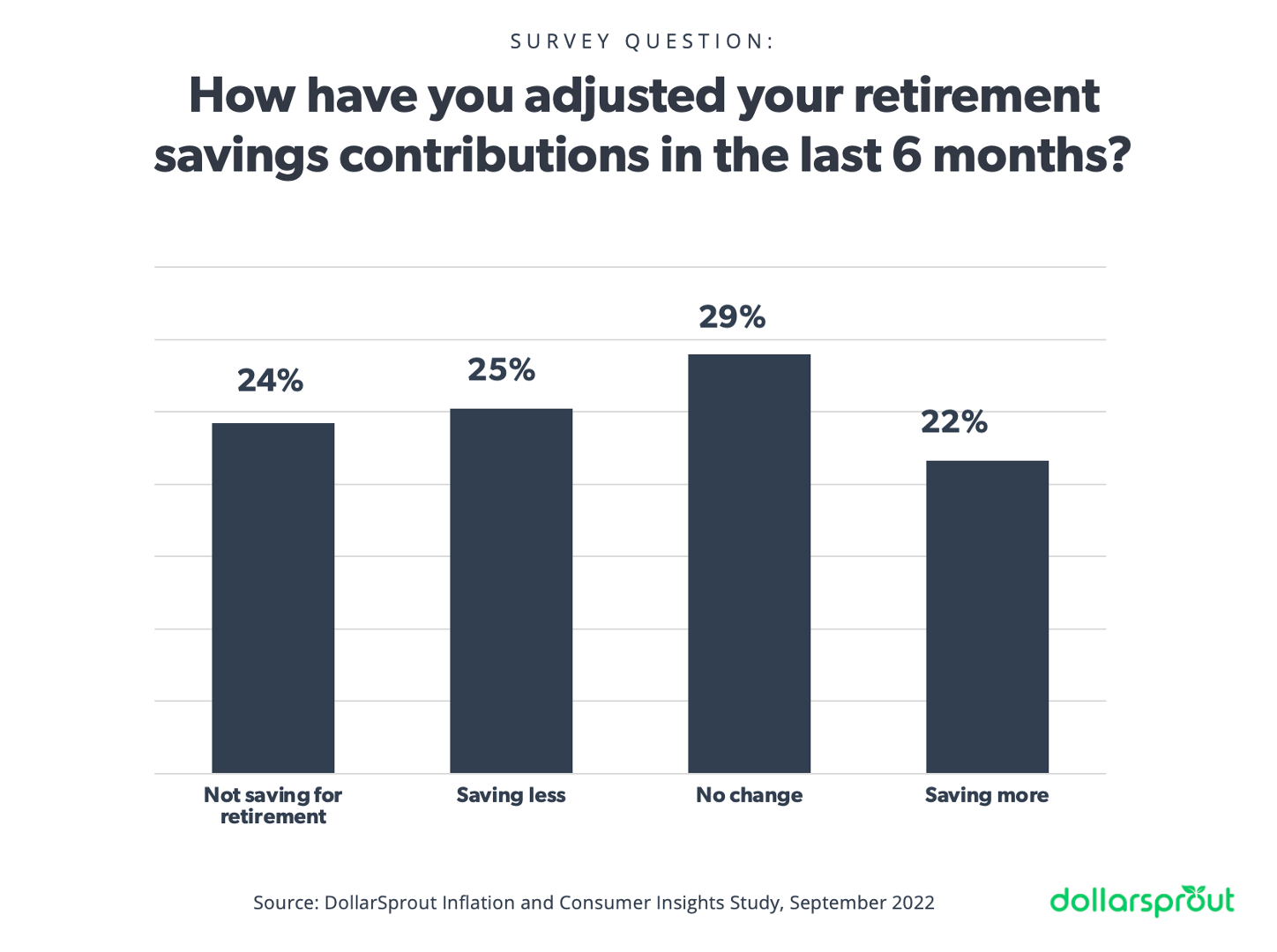

The outcomes weren’t precisely inspiring, however they weren’t precisely shocking both. The identical is true for our query about saving for retirement, the place 25% say they’re saving much less now and 24% say they don’t seem to be saving for retirement in any respect.